Betterment Editors

Meet our writer

Betterment Editors

Betterment’s editorial team draws on decades of combined experience to bring you clear, practical points of view on personal finance, investing, and long-term wealth. Together, we demystify money decisions, help you size up options, and share the knowledge needed to build wealth with confidence and ease.

Articles by Betterment Editors

-

![]()

How Betterment manages risks in your portfolio

How Betterment manages risks in your portfolio Jun 23, 2026 12:00:00 AM Betterment’s tools can keep you on track with the best chance of reaching your goals. Investing always involves some level of risk. But you should always have control over how much risk you take on. When your goals are decades away, it's easier to invest in riskier assets. The closer you get to reaching your goals, the more you may want to play it safe. Betterment’s tools can help manage risk and keep you on track toward your goals. In this guide, we’ll: Explain how Betterment provides allocation advice Talk about determining your personal risk level Walk through some of Betterment’s automated tools that help you manage risk Take a look at low-risk portfolios The key to managing your risk: asset allocation Risk is inherent to investing, and to some degree risk is good. High risk, high reward, right? What’s important is how you manage your risk. You want your investments to grow as the market fluctuates. One major way investors manage risk is through diversification. You’ve likely heard the old cliche, “Don’t put all your eggs in one basket.” This is the same reasoning investors use. We diversify our investments, putting our eggs in various baskets, so to speak. This way if one investment fails, we don’t lose everything. But how do you choose which baskets to put your eggs in? And how many eggs do you put in those baskets? Investors have a name for this process: asset allocation. Asset allocation involves splitting up your investment dollars across several types of financial assets (like stocks and bonds). Together these investments form your portfolio. A good portfolio will have your investment dollars in the right baskets: protecting you from extreme loss when the markets perform poorly, yet leaving you open to windfalls when the market does well. If that sounds complicated, there’s good news: Betterment will automatically recommend how to allocate your investments based on your individual goals. How Betterment provides allocation advice At Betterment, our recommendations start with your financial goals. Each of your financial goals—whether it’s a vacation or retirement—gets its own allocation primarily of stocks and bonds. Next we look at your investment horizon, a fancy term for “when you need the money and how you’ll withdraw it.” It’s like a timeline. How long will you invest for? Will you take it out all at once, or a little bit at a time? For a down payment goal, you might withdraw the entire investment after 10 years once you’ve hit your savings mark. But when you retire, you’ll probably withdraw from your retirement account gradually over the course of years. What if you don’t have a defined goal? If you’re investing without a timeline or target amount, we’ll use your age to set your investment horizon with a default target date of your 65th birthday. We’ll assume you’ll withdraw from it like a retirement account, but maintain a slightly riskier portfolio even when you hit the target date, since you haven’t decided when you'll liquidate those investments. But you’re not a “default” person. So why would you want a default investment plan? That’s why you should have a goal. When we know your goal and time horizon, we can determine the best risk level by assessing possible outcomes across a range of bad to average markets. Our projection model includes many possible futures, weighted by how likely we believe each to be. By some standards, we err on the side of caution with a fairly conservative allocation model. Our mission is to help you get to your goal through steady saving and appropriate allocation, rather than taking on unnecessary risk. How much risk should you take on? Your investment horizon is one of the most important factors in determining your risk level. The more time you have to reach your investing goals, the more risk you can afford to safely take. So generally speaking, the closer you are to reaching your goal, the less risk your portfolio should be exposed to. This is why we use the Betterment auto-adjust—a glide path (aka formula) used for asset allocation that becomes more conservative as your target date approaches. We adjust the recommended allocation and portfolio weights of the glide path based on your specific goal and time horizon. Want to take a more aggressive approach? More conservative? That’s totally ok. You’re in control. You always have the final say on your allocation, and we can show you the likely outcomes. Our quantitative approach helps us establish a set of recommended risk ranges based on your goals. If you choose to deviate from our risk guidance, we’ll provide you with feedback on the potential implications. Take more risk than we recommend, and we’ll tell you we believe your approach is “too aggressive” given your goal and time horizon. Even if you care about the downsides less than the average outcome, we’ll still caution you against taking on more risk, because it can be very difficult to recover from losses in a portfolio flagged as “too aggressive.” On the other hand, if you choose a lower risk level than our “conservative” band, we'll label your choice “very conservative.” A downside to taking a lower risk level is you may need to save more. You should choose a level of risk that’s aligned with your ability to stay the course. An allocation is only optimal if you’re able to commit to it in both good markets and bad ones. To ensure you’re comfortable with the short-term risk in your portfolio, we present both extremely good and extremely poor return scenarios for your selection over a one-year period. How Betterment automatically optimizes your risk An advantage of investing with Betterment is that our technology works behind the scenes to automatically manage your risk in a variety of ways, including auto-adjusted allocation and rebalancing. Auto-adjusted allocation For most goals, the ideal allocation will change as you near your goal. Our automated tools aim to make those adjustments as efficient and tax-friendly as possible. Deposits, withdrawals, and dividends can help us guide your portfolio toward the target allocation. And when selling any of your investments, our tax-smart technology is designed to minimize the potential tax impact. First we look for shares that have losses. These can offset other taxes. Then we sell shares with the smallest embedded gains (and smallest potential taxes). Rebalancing Over time, individual assets in a diversified portfolio move up and down in value, drifting away from the target weights that help achieve proper diversification. The difference between your target allocation and the actual weights in your current ETF portfolio is called portfolio drift. We define portfolio drift as the total absolute deviation of each super asset class from its target, divided by two. These super asset classes are US Bonds, International Bonds, Emerging Markets Bonds, US Stocks, International Stocks, and Emerging Markets Stocks. For Betterment-constructed portfolios that include a cash allocation, drift in the cash allocation is measured alongside super asset class drift. (Separately, Betterment-managed custom portfolios evaluate drift at the security group level. For reference, security groups are groupings of tickers that include a primary ticker, and may include secondary and/or tertiary tickers designed to help avoid wash sales and allow for tax-loss harvesting opportunities). A high drift may expose you to more (or less) risk than you intended when you set the target allocation. Betterment automatically monitors your account for rebalancing opportunities to reduce drift. There are several different methods depending on the circumstances: First, in response to cash flows such as deposits, withdrawals, and dividend reinvestments, Betterment buys underweight holdings and sells overweight holdings. This reactive rebalancing generally occurs when cash flows going into or out of the portfolio are already happening. We use inflows (like deposits and dividend reinvestments) to buy asset classes that are under-weight. This reduces the need to sell, which in turn reduces potential capital gains taxes. And we use outflows (like withdrawals) by seeking to first sell asset classes that are overweight. Second, if cash flows are not sufficient to keep a client’s portfolio drift within its applicable drift tolerance (such parameters as disclosed in Betterment’s Form ADV), automated rebalancing sells overweight holdings in order to buy underweight ones, aligning the portfolio more closely with its target allocation. This proactive rebalancing reshuffles assets that are already in the portfolio, and requires a minimum portfolio balance (clients can review the estimated balance at www.betterment.com/legal/portfolio-minimum). The rebalancing algorithm is also calibrated to avoid frequent small rebalance transactions and to seek tax efficient outcomes, such as helping to reduce wash sales and minimizing short-term capital gains. Allocation change rebalancing occurs when you change your target allocation. This sells securities and could possibly realize capital gains, but we still utilize our tax minimization algorithm to help reduce the tax impact. We’ll let you know the potential tax impact before you confirm your allocation change. Once you confirm it, we’ll rebalance to your new target with minimized drift. When Betterment rebalances a portfolio with a cash allocation, the rebalancing algorithm will first seek to bring the portfolio's cash allocation back to its target before investing in securities. If cash is below its target allocation, rebalancing will first use available funds (e.g., deposits, dividends, and/or proceeds from selling overweight holdings) to increase cash up to target, and only any remaining available cash is invested in securities; conversely, if cash is above its target allocation, the excess cash above target will be invested in securities as a part of the rebalancing transaction. If you are an Advised client, rebalancing in your account may function differently depending on the customizations your Advisor has selected for your portfolio. We recommend reaching out to your Advisor for further details. For more information, please review our rebalancing disclosures. How Betterment reduces risk in portfolios Investments like short-term US treasuries can help reduce risk in portfolios. At a certain point, however, including assets such as these in a portfolio no longer improves returns for the amount of risk taken. For Betterment, this point is our 60% stock portfolio. Portfolios with a stock allocation of 60% or more don’t incorporate these exposures. We include our U.S. Ultra-Short Income ETF and our U.S. Short-Term Treasury Bond ETF in the portfolio at stock allocations below 60% for both the IRA and taxable versions of the Betterment Core portfolio strategy. If your portfolio includes no stocks (meaning you allocated 100% of your portfolio’s investments to bonds), we can take the hint. You likely don’t want to worry about market volatility. So in that case, we recommend that you invest everything in these ETFs. At 0% stocks, a Betterment Core portfolio generally consists of 60% U.S. short-term treasury bonds, 20% U.S. short-term high quality bonds, and 20% inflation protected bonds.* Increase the stock allocation in your portfolio, and we’ll decrease the allocation to these exposures. Reach the 60% stock allocation threshold, and we’ll remove these funds from the recommended portfolio. At that allocation, they decrease expected returns given the desired risk of the overall portfolio. Short-term U.S. treasuries generally have lower volatility (any price swings are quite mild) and smaller drawdowns (shorter, less significant periods of loss). The same can be said for short-term high quality bonds, but they are slightly more volatile. It’s also worth noting that these asset classes don’t always go down at exactly the same time. By combining these asset classes, we’re able to produce a portfolio with a higher potential yield while maintaining relatively lower volatility. As with other assets, the returns for assets such as high quality bonds include both the possibility of price returns and income yield. Generally, price returns are expected to be minimal, with the primary form of returns coming from the income yield. The yields you receive from the ETFs in Betterment’s 0% stocks portfolio are the actual yields of the underlying assets after fees. Since we’re investing directly in funds that are paying prevailing market rates, you can feel confident that the yield you receive is fair and in line with prevailing rates. Work toward your financial goals without risking it all Choosing an investment portfolio is a personal decision, but it doesn’t have to be a difficult one. At Betterment, our goal is to help you feel confident that you’re always taking an appropriate amount of risk. We’ll help you select a portfolio with the risk level that’s right for you, and you can rest assured that our automated services are built to manage it efficiently. *Target investments, actual holdings will vary. -

![]()

Inside the investing kitchen, part 1

Inside the investing kitchen, part 1 Jun 8, 2026 12:00:00 AM The recipe for a better portfolio, and the science behind a safer nest egg. Jamie Lee isn’t a Top Chef, but he knows his way around the kitchen. He dabbles in sous vide with the help of a sous chef (his 6-year-old daughter). He loves smoking salmon low and slow on a pair of pellet grills. And in some ways, his day job on the Betterment Investing team resembles the culinary world as well. He and his teammates work in a test kitchen of sorts, defining and refining the recipes for our low-cost and globally-diversified portfolios. They size up ingredients, pair flavors, and thoughtfully assemble the courses of each “meal.” All in service of customers with varying appetites for risk. It's highly-technical work, but we wouldn't be Betterment if we didn't make our methodologies as accessible as possible. So whether you're kicking the tires on our services, or you're already a customer and simply curious about the mechanics of your money machine, come along for a three-part, behind-the-scenes look at how we cook up a better portfolio. Here in part 1, we'll explore how we allocate your investing at a high level. In part 2, we'll zoom in to our process for selecting specific funds. And in part 3, we'll show you how we handle thousands of trades each day to keep our customers’ portfolios in tip-top shape. The science behind a safer nest egg Betterment customers rely on Jamie and team to do the heavy lifting of portfolio construction. They distill handfuls of asset classes, a hundred-plus risk levels, and thousands of funds into a simple yet eclectic menu of investment options. This process applies to the invested (non-cash) portion of our portfolios, and underpinning much of it is something called Modern Portfolio Theory, a framework developed by the late American economist Harry Markowitz. The theory revolutionized how investors think about risk, and led to Markowitz winning the Nobel Prize in 1990. Diversification lies at the heart of Modern Portfolio Theory. The more of it your investing has, the theory goes, the less risk you're exposed to. But that barely scratches the surface. One of the meatiest parts of building a portfolio (and by extension, diversifying your investing) is how much weight to give each asset class, also known as asset allocation. Broadly speaking, you have stocks and bonds. But you can slice up the pie in several other ways. There’s large cap companies or less established ones. Government debt or the corporate variety. And even more relevant as of late: American markets or international. Jamie came of age in South Korea during the late 90s. Back here in the States, the dot-com bubble was still years away from popping. But in South Korea and Asia more broadly, a financial crisis was well underway. And it changed the trajectory of Jamie’s career. His interest in and application of math shifted from computer science to the study of markets, and ultimately led to a PhD in statistics. Jamie Lee (right) helps optimize the weights of asset classes in Betterment portfolios. For Jamie, the interplay of markets at a global level is fascinating. So it’s only fitting that when optimizing asset allocations for customers, Jamie and team start with the hypothetical "global market portfolio," an imaginary snapshot of all the investable assets in the world. The current value of U.S. stocks, for example, represents about two-thirds the value of all stocks, so it's weighted accordingly in the global market portfolio. These weights are the jumping off point for a key part of the portfolio construction process: projecting future returns. Reverse engineering expected returns “Past performance does not guarantee future results.” We include this type of language in all of our communications at Betterment, but for quantitative researchers, or “quants,” like Jamie, it’s more than a boilerplate. It’s why our forecasts for the expected returns of various asset classes largely aren't based on historical performance. They're forward-looking. "Past data is simply too unreliable," says Jamie. "Look at the biggest companies of the 90s; that list is completely different from today.” So to build our forecasts, commonly referred to in the investing world as Capital Market Assumptions, we pretend for a moment that the global market portfolio is the optimal one. Since we know roughly how each of those asset classes performs relative to one another, we can reverse engineer their expected returns. This robust math is represented by a deceivingly short equation—μ = λ Σ ωmarket—which you can read more about in our full portfolio construction methodology. From there, we simulate thousands of paths for the market, factoring in both our forecasts and those of large asset managers like BlackRock to find the optimal allocation for each path. Then we average those weights to land on a single recommendation. This “Monte Carlo" style of simulations is commonly used in environments filled with variables. Environments like, say, capital markets. The outputs are the asset allocation percentages (refreshed each year) that you see in the holdings portion of your portfolio details. At this point in the journey, however, our Investing team's work is hardly finished. They still need to seek out some of the most cost-effective, and just plain effective, funds that give you the intended exposure to each relevant asset class. For this, we need to head out of the test kitchen and into the market. So don’t forget your tote bag. -

![]()

How we keep your Betterment account and investments safe

How we keep your Betterment account and investments safe Jun 3, 2026 12:15:00 AM So you can invest with peace of mind All investing comes with some risk. But that risk should be based on the market, not your broker. That’s why we safeguard both your Betterment account and your investments with multiple security measures, all so you can log in and invest or save with peace of mind. Here’s a sampling. Four ways we keep your Betterment account safe Two-factor authentication Two-factor authentication (2FA) adds an extra layer of security to your account, like an extra lock on a door. Besides your regular password, 2FA requires a second form of verification such as a code texted to your phone (good) or one served up by an authenticator app like Google Authenticator (even more secure). This helps ensure that even if someone manages to get hold of your Betterment password, they still can't access your account without a second form of verification. Encryption Every time you interact with us, whether on our website or our app, your data is protected by encrypted connections. This means that the information transmitted between your device and our servers is scrambled in a way that only we can understand. Password hashing When you create a password for your Betterment account, it's not stored in plain text. Instead, we use a process called hashing, which converts your password into a unique string of characters. This way, even if our systems were breached, your actual password would remain unknown and unusable by unauthorized parties. App passwords Connecting third-party apps to your Betterment account (or vice versa) unlocks several benefits. You can easily track your net worth on Betterment, for example. Or quickly import your Betterment tax forms to certain tax prep software. When a third-party app asks for your Betterment credentials, instead of using your regular login, we ask you to create a password specifically for that app. In the scenario the third-party app’s connection is compromised, you can easily revoke its read-only access to your Betterment account. Note that some apps may use the OAuth standard, which lets you use your regular login while maintaining a similar level of security as an app password. TurboTax is one such example. Four ways we keep your investments safe Easy verification of holdings Transparency is one of our key principles, so we make it easy to verify everything is in its right place. We not only show each trade made on your behalf and the precise number of shares in which you’re invested, we also list each fractional share sold and the respective gross proceeds and cost basis for each. You can find all this information in the Holdings and Activity tabs for each of your goals. Independent oversight We regularly undergo review by independent auditors. This means auditors reconcile every share and every dollar we say we have against our actual holdings. They also spot check random customer accounts and verify that account statements match our internal records. And they ask questions if anything is even a penny off. No commingling of funds Your funds are kept separate from Betterment’s operational funds. This means that your investments are held in your name and are never mixed with our company finances. In the unlikely event we face financial difficulties, your assets remain secure and untouched. SIPC Coverage Betterment Securities is a member of SIPC, which protects securities customers of its members up to $500,000 (including $250,000 for claims for cash). Explanatory brochure available upon request or at www.sipc.org. How you can help Be on the lookout for suspicious phone calls, texts, and emails (odd-looking URLs, typo-riddled messages, etc.) and know that Betterment will never ask you for your password or 2FA code except when logging in or editing your personal information in the app. Use a strong, unique password for your account. If you receive any unexpected or suspicious communications or have questions, please email fraud@betterment.com. -

![]()

Security Incident Report: January 2026

Security Incident Report: January 2026 Mar 30, 2026 11:13:32 AM Executive Summary Transparency, trust and the safety of our customers' assets are our highest priorities at Betterment. Consistent with those priorities, we are sharing details following the conclusion of our investigation into the January 9 security incident. What Happened On January 9, 2026, an unauthorized third-party (“threat actor”) gained access to a Betterment employee’s account through social engineering. This access included applications we use for marketing and operations. Customer account and transaction systems were not impacted. In addition to other controls, those systems are protected by device trust policies, which restrict access to Betterment-managed devices only, regardless of whether valid credentials are presented. This additional layer of security protected customer accounts, and transaction systems were never breached. Our investigation confirmed that no customer accounts, passwords, or login information were compromised. The threat actor sent a fraudulent crypto offer to approximately 460,000 customers via email and mobile push notifications. We immediately intervened to revoke access and alerted those customers to disregard the offer. We made those impacted by the offer whole for their losses. Impact and Data Security Before the threat actor’s activity was suspended, they were able to obtain data associated with approximately 1.4 million customers and business contacts. In the vast majority of cases, the data was limited to name only or name in combination with email address. Next Steps We’ve taken this opportunity to reinforce our systems and enhance our security protocols, ensuring our protections remain as resilient as possible. This includes enhancements to our existing multi-factor authentication (“MFA”) login controls and security monitoring. Additional details are outlined in “Control Enhancements” below. Post-Incident Response Investigation Upon detection, we immediately activated our incident response plan and launched an investigation. We engaged external counsel to lead the investigation with the support of CrowdStrike, an experienced forensics firm. The investigation was also supported by HaystackID, an independent data analytics firm, which reviewed data that was accessed to identify potential privacy risks. Response to Extortion Attempt Several days after the initial incident, we received communications from a criminal group who demanded a crypto payment. Additional harassment and threatening messages followed, with conflicting deadlines. We engaged professional advice and consulted with law enforcement, and decided not to engage with the criminal group. On January 23, the criminal group posted data obtained in this incident to a since-removed leak site online. Betterment Communications On January 9, we quickly alerted customers who received the fraudulent crypto offer to disregard it. On January 12, email communications were sent to all customers alerting them to the incident, and we established a customer update page. Since then, we have posted updates to this page as the investigation unfolded. Throughout our investigation, we worked closely with law enforcement, including promptly reporting the incident to various law enforcement agencies and filing an Internet Crime Complaint Center (“IC3”) report. We also shared timely threat intelligence and indicators of compromise (“IOCs”) with the security community. Once our privacy assessment concluded, we sent notifications to a limited subset of customers whose impacted information included a combination of data that could be more sensitive. Control Enhancements Betterment has taken several steps to harden its security posture and mitigate the risk of similar incidents in the future, including: Strengthened existing multi-factor authentication (“MFA”) login controls by sunsetting all remaining non-hardware methods and further restricting enrollment of new authenticators Enhanced our security monitoring and alerting processes to enable faster detection and response to potentially unauthorized activity Reinforced existing phishing simulation and security awareness training Deployed advanced Denial of Service (DoS) protection to handle larger and more-sophisticated attacks While these improvements are important, we are not stopping here. We continue to evaluate and adopt additional enhancements to further strengthen controls and overall security posture. Customer & Partner Guidance Betterment accounts are protected by multiple layers of security; no customer action is required. We do encourage all customers to remain vigilant and to be cautious of unexpected communications. Please remember that Betterment will never call, text, or email you with a request to share your password or other sensitive personal information. No additional actions are required from Betterment at Work 401(k) plan sponsors or third-party advisors that manage client assets through the Betterment Advisor Solutions platform. The threat actor did not have access to API keys, payroll integrations, or other system interfaces. If customers ever suspect unauthorized activity or have any concerns about fraud, our team can be reached at fraud@betterment.com. Conclusion To be clear, this is not the experience we want for our customers and partners. We continue to take steps to add additional layers of security and improve our protections to consistently earn and live up to the trust our customers place in Betterment every day. Appendix: Timeline Jan 09, 13:31 EST Initial Compromise: Social engineering techniques including the use of falsified caller ID (labeled “Betterment IT”) and a voice phishing kit were deployed to obtain credentials and a required multi-factor authentication one-time passcode. The threat actor used the resulting credentials and MFA authentication to establish a new registered device, allowing them to access the Okta Single Sign-on portal from their own computer. Jan 09, 13:31-18:18 Unauthorized Activity: The threat actor accessed several web applications used for marketing and operations; in addition to other controls, transaction systems were protected by device trust policies, which restrict access to Betterment-managed devices only. Before the threat actor’s activity was suspended, they were able to obtain data associated with approximately 1.4 million customers and business contacts. In the vast majority of cases, the data was limited to name only or name in combination with email address. The threat actor was not able to establish persistence, lateral movement, or privilege escalation, and did not impact the integrity of any systems. Jan 09, 17:46 Fraudulent Crypto Promotion / Detection: The threat actor sent a fraudulent, crypto-related message that appeared to come from Betterment to approximately 460,000 customers. Jan 09, 18:03 Incident Response: Betterment personnel declared an incident and began response protocols. Jan 09, 18:05 Containment: The user account within the third-party marketing application was suspended. Jan 09, 18:09 The Okta Universal Directory account used by the threat actor was de-activated, and active sessions canceled. Jan 09, 18:18 Following the threat actor's access to the account being revoked, all activity was suspended. Jan 09, 19:00 Initial communication: Betterment’s first customer communication was emailed and posted to social media, alerting customers about the fraudulent crypto offer. Beginning Jan 09 Professional services: We engaged external legal counsel and, through them, the cybersecurity firm CrowdStrike for forensic investigation, and the independent data analytics firm HaystackID to assess privacy impact. Jan 12, 10:00 Additional Communication: We emailed all customers to make them aware of the security incident, regardless of whether they received the crypto email. We also established a page to provide ongoing updates. Jan 12, 10:39 Demand: Betterment received communications from a criminal group demanding a crypto payment. We engaged with law enforcement and threat intelligence specialists to seek advice regarding the appropriate response strategy. Jan 13, 9:04 Denial of Service: Betterment experienced intermittent outages of our website and mobile app due to a distributed denial-of-service (DDoS) attack. We began mitigation efforts immediately, restoring partial access by 10:25 EST and full access across all services by 14:40 EST. Jan 14 through Jan 16 Targeted Threats: During this period, certain Betterment employees were subject to threatening messages and harassment believed to be related to the ongoing incident. We worked with law enforcement and security partners to assess and respond. No Betterment systems were impacted as a result of these activities. Jan 23 Data publication: Data originating from the incident was temporarily published to a “leak site” on a .onion domain, which has since been removed. -

![]()

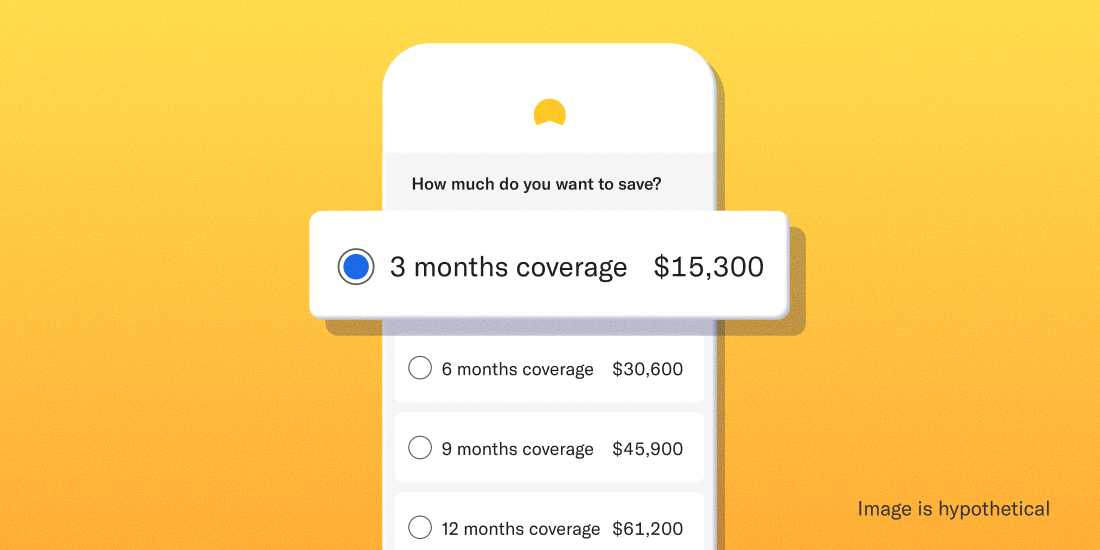

Three steps to size up your emergency fund

Three steps to size up your emergency fund Dec 3, 2025 6:00:00 AM Strive for at least three months of expenses while taking these factors into consideration. Imagine losing your job, totaling your car, or landing in the hospital. How quickly would your mind turn from the shock of the event itself to worrying about paying your bills? If you’re anything like the majority of Americans recently surveyed by Bankrate, finances would add insult to injury pretty fast: Only around 2 in 5 Americans would pay for an emergency from their savings In these scenarios, an emergency fund can not only help you avoid taking on high-interest debt or backtracking on other money goals, it can give you one less thing to worry about in trying times. So how much should you have saved, and where should you put it? Follow these three steps. 1. Tally up your monthly living expenses — or use our shortcut. Coming up with this number isn’t always easy. You may have dozens of regular expenses falling into one of a few big buckets: Food Housing Transportation Medical When you create an Emergency Fund goal at Betterment, we automatically estimate your monthly expenses based on two factors from your financial profile: Your self-reported household annual income Your zip code’s estimated cost of living You’re more than welcome to use your own dollar figure, but don’t let math get in the way of getting started. 2. Decide how many months make sense for you We recommend having at least three months’ worth of expenses in your emergency fund. A few scenarios that might warrant saving more include: You support others with your income Your job security is iffy You don’t have steady income You have a serious medical condition But it really comes down to how much will help you sleep soundly at night. According to Bankrate’s survey, nearly ⅔ of people say that total is six months or more. Whatever amount you land on, we’ll suggest a monthly recurring deposit to help you get there. We’ll also project a four-year balance based on your initial and scheduled deposits and your expected return and volatility. Why four years? We believe that’s a realistic timeframe to save at least three months of living expenses through recurring deposits. If you can get there quicker and move on to other money goals, even better! 3. Pick a place to keep your emergency fund We recommend keeping your emergency fund in one of two places: cash—more specifically a low-risk, high-yield cash account—or a bond-heavy investing account. A low-risk, high-yield cash account like our Cash Reserve may not always keep pace with inflation, but it comes with no investment risk. Cash Reserve offered by Betterment LLC and requires a Betterment Securities brokerage account. Betterment is not a bank. FDIC insurance provided by Program Banks, subject to certain conditions. Learn more. An investing account is better suited to keep up with inflation but is relatively riskier. Because of this volatility, we currently suggest adding a 30% buffer to your emergency fund’s target amount if you stick with the default stock/bond allocation. There also may be tax implications should you withdraw funds. Your decision will again come down to your comfort level with risk. If the thought of seeing your emergency fund’s value dip, even for a second, gives you heartburn, you might consider sticking with a cash account. Or you can always hedge and split your emergency fund between the two. There’s no wrong answer here! Remember to go with the (cash) flow There’s no final answer here either. Emergency funds naturally ebb and flow over the years. Your monthly expenses could go up or down. You might have to withdraw (and later replace) funds. Or you simply might realize you need a little more saved to feel secure. Revisit your numbers on occasion—say, once a year or anytime you get a raise or big new expense like a house or baby—and rest easy knowing you’re tackling one of the most important financial goals out there. -

![]()

Self-directed investing, the Betterment way

Self-directed investing, the Betterment way Nov 11, 2025 7:00:00 AM See what makes Betterment’s self-directed investing different from the rest. Plus, get three tips to help develop your own investing strategy. Key takeaways We surveyed our customers and learned that 75% of them use self-directed investing elsewhere, but many want it alongside their automated investing—so we built it the Betterment way. With Betterment, you can invest your way, buying and selling thousands of stocks and ETFs with no commissions. Manage your automated portfolios, cash accounts, and self-directed trades together on one platform for a fuller view of your finances. Unlike other investing apps, Betterment’s tax impact preview lets you see the impact of a sale before you trade, so there are no tax surprises. Invest smarter with these three tips: set clear goals, plan for taxes, and keep emotions out of your investing. Recently, we surveyed our customers and learned that 75% of them use some form of self-directed investing. That was eye-opening. While our automated investing tools are designed to take the work out of wealth building, many people still want the option to pick and manage certain investments on their own. So we asked ourselves: how can we bring self-directed investing to life—the Betterment way? Our answer: combine our award-winning platform with a customer-first experience to let you buy and sell thousands of stocks and ETFs with no commissions. With Betterment’s self-directed investing, you’ll get more investing choices, the ability to see all of your investments in a consolidated place, and tax insights you won’t find anywhere else. Investing your way, all in one place Not everyone invests for the same reason. We know this because we continually solicit feedback from our customers. Some customers told us they want to invest in companies they believe in. Others find it intellectually rewarding to follow markets and make trades. And many simply like having more control over their portfolio. With Betterment’s self-directed investing, you can get that flexibility while keeping everything on one platform. Manage your automated portfolios, cash accounts, and self-directed trades side by side, with technology designed to give you a clear view of your financial life. Tax insights you won’t get anywhere else Here’s where we’re really different than the typical “stock trading” platforms. Self-directed trading often means more frequent buying and selling, which can bring a hefty and unexpected tax bill at the end of the year that catches people off guard. In fact, when we asked our customers about their biggest challenge with self-directed investing on other apps, the top answer was “managing tax implications.” We solved that challenge. At Betterment, you’ll see a tax impact preview before you sell a stock or ETF. That preview includes how the sale could affect your taxes, and even potential wash sales. A wash sale occurs when you sell a security at a loss and then repurchase the same or a substantially identical security within 30 days before or after the sale, disallowing the tax deduction for that loss. With our tax impact preview, there are no surprises or guesswork. Just clear tax insights to help you make smarter decisions. (See how tax impact preview works.) Three tips to get started with self-directed investing Self-directed investing provides you with the choice to invest your way. But you get to decide what “your way” means. To help, here are three steps to get started: Have a clear goal before you trade: Don’t just buy because something looks hot or is in the news. Ask yourself: Am I investing for long-term growth, short-term income, diversification, or some other reason? Having a clear purpose can help you avoid making impulsive trades. Think about taxes before you sell: Selling a stock or ETF can trigger capital gains taxes. Short-term gains (for investments held less than a year) are usually taxed at a higher rate than long-term gains. Using tools that preview your tax impact before you trade—like Betterment’s—can help you avoid surprises. Avoid emotional trading: Markets move fast. It’s easy to panic-sell when prices dip or chase a stock that’s soaring. Instead, set rules for yourself—like only initiating a trade at pre-set price targets or sticking to a dollar-cost averaging plan—so emotions don’t dictate your decisions. Plus, at Betterment, your trades are queued for execution and not made immediately, but they are made in a timely manner, limiting your ability to try to “time the market.” -

![]()

What’s an IRA and how does it work?

What’s an IRA and how does it work? Nov 7, 2025 7:00:00 AM Learn more about this investment account with tax advantages that help you prepare for retirement. An Individual Retirement Account (IRA) is a type of investment account with tax advantages that helps you prepare for retirement. Depending on the type of IRA you invest in, you can make tax-free withdrawals when you retire, earn tax-free interest, or put off paying taxes until retirement. The sooner you start investing in an IRA, the more time you have to accrue interest before you reach retirement age. But an IRA isn’t the only kind of investment account for retirement planning. And there are multiple types of IRAs available. If you’re planning for retirement, it’s important to understand your options and learn how to maximize your tax benefits. If your employer offers a 401(k), it may be a better option than investing in an IRA. While anyone can open an IRA, employers typically match a portion of your contribution to a 401(k) account, helping your investment grow faster. In this article, we’ll walk you through: What makes an IRA different from a 401(k) The types of IRAs How to choose between a Roth IRA and a Traditional IRA Timing your IRA contributions IRA recharacterizations Roth IRA conversions Let’s start by looking at what makes an Individual Retirement Account different from a 401(k). How is an IRA different from a 401(k)? When it comes to retirement planning, the two most common investment accounts people talk about are IRAs and 401(k)s. 401(k)s offer similar tax advantages to IRAs, but not everyone has this option. Anyone can start an IRA, but a 401(k) is what’s known as an employer-sponsored retirement plan. It’s only available through an employer. Other differences between these two types of accounts are that: Employers often match a percentage of your contributions to a 401(k) 401(k) contributions come right out of your paycheck 401(k) contribution limits are significantly higher If your employer matches contributions to a 401(k), they’re basically giving you free money you wouldn’t otherwise receive. It’s typically wise to take advantage of this match before looking to an IRA. With an Individual Retirement Account, you determine exactly when and how to make contributions. You can put money into an IRA at any time over the course of the year, whereas a 401(k) almost always has to come from your paycheck. Note that annual IRA contributions can be made up until that year’s tax filing deadline, whereas the contribution deadline for 401(k)s is at the end of each calendar year. Learning how to time your IRA contributions can significantly increase your earnings over time. Every year, you’re only allowed to put a fixed amount of money into a retirement account, and the exact amount often changes year-to-year. For an IRA, the contribution limit for 2026 is $7,500 if you’re under 50, or $8,600 if you’re 50 or older. For a 401(k), the contribution limit for 2026 is $24,500 if you’re under 50, or $32,500 if you’re 50 or older. These contribution limits are separate, so it’s not uncommon for investors to have both a 401(k) and an IRA. And as a side note for those 50 or older, starting in 2026, 401(k) catch-up contributions must go into a Roth 401(k) specifically if you received more than $145,000 in FICA wages (salaries, commissions, etc.) the prior year. What are the types of IRAs? The challenge for most people looking into IRAs is understanding which kind of IRA is most advantageous for them. For many, this boils down to Roth and/or Traditional. The advantages of each can shift over time as tax laws and your income level changes, so this is a common periodic question for even advanced investors. As a side note, there are other IRA options suited for the self-employed or small business owner, such as the SEP IRA, but we won’t go into those here. As mentioned in the section above, IRA contributions are not made directly from your paycheck. That means that the money you are contributing to an IRA has already been taxed. When you contribute to a Traditional IRA, your contribution may be tax-deductible. Whether you are eligible to take a full, partial, or any deduction at all depends on if you or your spouse is covered by an employer retirement plan (i.e. a 401(k)) and your income level (more on these limitations later). Once funds are in your Traditional IRA, you will not pay any income taxes on investment earnings until you begin to withdraw from the account. This means that you benefit from “tax-deferred” growth. If you were able to deduct your contributions, you will pay income tax on the contributions as well as earnings at the time of withdrawal. If you were not eligible to take a deduction on your contributions, then you generally will only pay taxes on the earnings at the time of withdrawal. This is done on a “pro-rata” basis. Comparatively, contributions to a Roth IRA are not tax deductible. When it comes time to withdraw from your Roth IRA, your withdrawals will generally be tax free—even the interest you’ve accumulated. How to choose between a Roth IRA and a Traditional IRA For most people, choosing an Individual Retirement Account is a matter of deciding between a Roth IRA and a Traditional IRA. Neither option is inherently better: it depends on your income and your tax bracket now and in retirement. Your income determines whether you can contribute to a Roth IRA, and also whether you are eligible to deduct contributions made to a Traditional IRA. However, the IRS doesn’t use your gross income; they look at your modified adjusted gross income, which can be different from taxable income. With Roth IRAs, your ability to contribute is phased out when your modified adjusted gross income (MAGI) reaches a certain level. If you’re eligible for both types of IRAs, the choice often comes down to what tax bracket you’re in now, and what tax bracket you think you’ll be in when you retire. If you think you’ll be in a lower tax bracket when you retire, postponing taxes with a Traditional IRA will likely result in you keeping more of your money. If you expect to be in a higher tax bracket when you retire, using a Roth IRA to pay taxes now may be the better choice. The best type of account for you may change over time, but making a choice now doesn’t lock you into one option forever. So as you start retirement planning, focus on where you are now and where you’d like to be then. It’s healthy to re-evaluate your position periodically, especially when you go through major financial transitions such as getting a new job, losing a job, receiving a promotion, or creating an additional revenue stream. Timing IRA contributions: why earlier is better Regardless of which type of IRA you select, it helps to understand how the timing of your contributions impacts your investment returns. It’s your choice to either make a maximum contribution early in the year, contribute over time, or wait until the deadline. By timing your contribution to be as early as possible, you can maximize your time in the market, which could help you gain more returns over time. Consider the difference between making a maximum contribution on January 1 and making it on December 1 each year. Then suppose, hypothetically, that your annual growth rate is 10%. Here’s what the difference could look like between an IRA with early contributions and an IRA with late contributions: This figure represents the scenarios mentioned above.‘Deposit Early’ indicates depositing $6,000 on January 1 of each calendar year, whereas ‘Deposit Late’ indicates depositing $6,000 on December 1 of the same calendar year, both every year for a ten-year period. Calculations assume a hypothetical growth rate of 10% annually. The hypothetical growth rate is not based on, and should not be interpreted to reflect, any Betterment portfolio, or any other investment or portfolio, and is purely an arbitrary number. Further, the results are solely based on the calculations mentioned in the preceding sentences. These figures do not take into account any dividend reinvestment, taxes, market changes, or any fees charged. The illustration does not reflect the chance for loss or gain, and actual returns can vary from those above. What’s an IRA recharacterization? You might contribute to an IRA before you have started filing your taxes and may not know exactly what your Modified Adjusted Gross Income will be for that year. Therefore, you may not know whether you will be eligible to contribute to a Roth IRA, or if you will be able to deduct your contributions to a Traditional IRA. In some cases, the IRS allows you to reclassify your IRA contributions. A recharacterization changes your contributions (plus the gains or minus the losses attributed to them) from a Traditional IRA to a Roth IRA, or, from a Roth IRA to a Traditional IRA. It’s most common to recharacterize a Roth IRA to a Traditional IRA. Generally, there are no taxes associated with a recharacterization if the amount you recharacterize includes gains or excludes dollars lost. Here are three instances where a recharacterization may be right for you: If you made a Roth contribution during the year but discovered later that your income was high enough to reduce the amount you were allowed to contribute—or prohibit you from contributing at all. If you contributed to a Traditional IRA because you thought your income would be above the allowed limits for a Roth IRA contribution, but your income ended up lower than you’d expected. If you contributed to a Roth IRA, but while preparing your tax return, you realize that you’d benefit more from the immediate tax deduction a Traditional IRA contribution would potentially provide. Additionally, we have listed a few methods that can be used to correct an over-contribution to an IRA in this FAQ resource. You cannot recharacterize an amount that’s more than your allowable maximum annual contribution. You have until each year’s tax filing deadline to recharacterize—unless you file for an extension or you file an amended tax return. What’s a Roth conversion? A Roth conversion is a one-way street. It’s a potentially taxable event where funds are transferred from a Traditional IRA to a Roth IRA. There is no such thing as a Roth to Traditional conversion. It is different from a recharacterization because you are not changing the type of IRA that you contributed to for that particular year. There is no cap on the amount that’s eligible to be converted, so the sky’s the limit for those that choose to convert. We go into Roth conversions in more detail in our Help Center. -

![]()

Your Betterment experience has just undergone a major upgrade

Your Betterment experience has just undergone a major upgrade Aug 18, 2025 9:57:03 AM A better way to manage your money is here. Your Betterment experience has just undergone a major upgrade, built around one idea: making managing your money more flexible and intuitive. We’ve redesigned how your accounts and goals work together, so you can organize your money the way that makes the most sense for you. What changed—and why? We’ve always believed in goal-based investing. It’s what sets Betterment apart. But in the past, each goal in Betterment was tied to a single account. That worked when needs were simpler. But you asked for more flexibility to reflect your financial life, and we’ve delivered. Now, by separating account data from goal advice, we’ve created space for more personalized guidance, clearer navigation, and more flexibility for you and your money. What you’ll see that’s new today: A cleaner design: A modern look that surfaces what matters most—no more digging through tabs. A dedicated page for each goal: Get personalized advice, projections, and next steps, all in one place. A streamlined overview of single accounts: See balances, holdings, and performance clearly, while being able to click through directly to access account details. A dedicated goal forecaster: Get insights in one place to see how actions may affect future earnings. And as a BONUS: Your Activity Page got an upgrade 🔄 Enjoy a clearer window into trades, transfers, and transactions. And we’re just getting started. We’re already building the next phase of features to make your Betterment experience more powerful and flexible. Multiple accounts in one goal: Get combined advice across different account types and tax treatments. Smarter, goal-specific advice: We’ll help you optimize every dollar for what you care about most. Shared goals: Soon, you’ll be able to co-own a goal with another Betterment user. More tailored investing guidance: Tell us your goal, and we’ll recommend the best path to get there. A faster, more user-friendly Betterment experience. To better fit your financial needs, we’ve separated account data from goal-based advice to give you more control and a better sense of ownership over your account. Whether you're planning for retirement, building an emergency fund, or simply growing your wealth through automated investing, Betterment is now better built for how you’ll manage your money. Smarter tools, personalized advice, and goal-based investing—all working together for you.