Three steps to size up your emergency fund

Strive for at least three months of expenses while taking these factors into consideration.

Imagine losing your job, totaling your car, or landing in the hospital. How quickly would your mind turn from the shock of the event itself to worrying about paying your bills?

If you’re anything like the majority of Americans recently surveyed by Bankrate, finances would add insult to injury pretty fast:

Only around 2 in 5 Americans would pay for an emergency from their savings

In these scenarios, an emergency fund can not only help you avoid taking on high-interest debt or backtracking on other money goals, it can give you one less thing to worry about in trying times.

So how much should you have saved, and where should you put it? Follow these three steps.

1. Tally up your monthly living expenses — or use our shortcut.

Coming up with this number isn’t always easy. You may have dozens of regular expenses falling into one of a few big buckets:

- Food

- Housing

- Transportation

- Medical

When you create an Emergency Fund goal at Betterment, we automatically estimate your monthly expenses based on two factors from your financial profile:

- Your self-reported household annual income

- Your zip code’s estimated cost of living

You’re more than welcome to use your own dollar figure, but don’t let math get in the way of getting started.

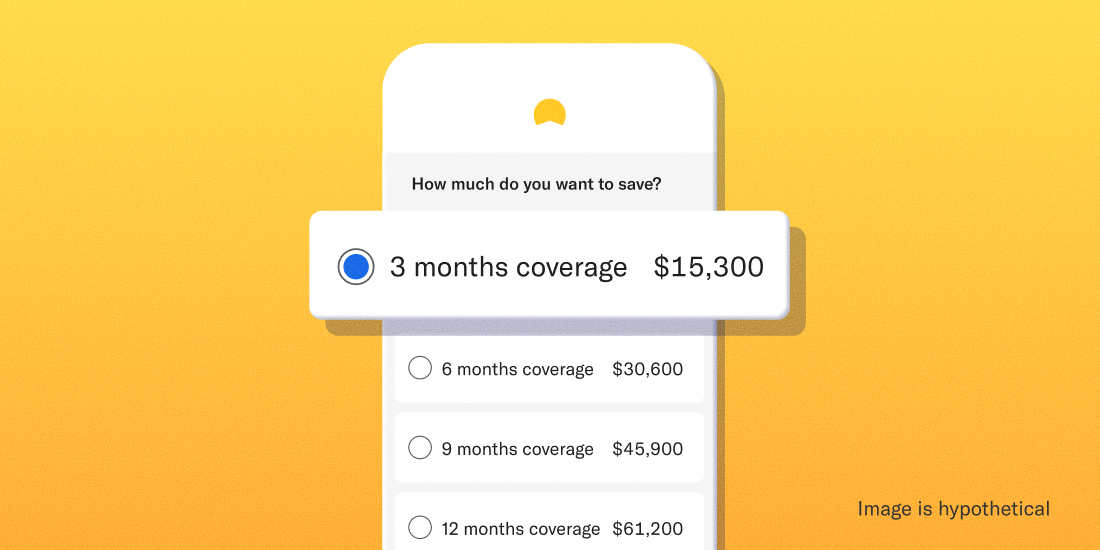

2. Decide how many months make sense for you

We recommend having at least three months’ worth of expenses in your emergency fund. A few scenarios that might warrant saving more include:

- You support others with your income

- Your job security is iffy

- You don’t have steady income

- You have a serious medical condition

But it really comes down to how much will help you sleep soundly at night. According to Bankrate’s survey, nearly ⅔ of people say that total is six months or more.

Whatever amount you land on, we’ll suggest a monthly recurring deposit to help you get there. We’ll also project a four-year balance based on your initial and scheduled deposits and your expected return and volatility.

Why four years? We believe that’s a realistic timeframe to save at least three months of living expenses through recurring deposits. If you can get there quicker and move on to other money goals, even better!

3. Pick a place to keep your emergency fund

We recommend keeping your emergency fund in one of two places: cash—more specifically a low-risk, high-yield cash account—or a bond-heavy investing account.

- A low-risk, high-yield cash account like our Cash Reserve may not always keep pace with inflation, but it comes with no investment risk.

Cash Reserve offered by Betterment LLC and requires a Betterment Securities brokerage account. Betterment is not a bank. FDIC insurance provided by Program Banks, subject to certain conditions. Learn more.

- An investing account is better suited to keep up with inflation but is relatively riskier. Because of this volatility, we currently suggest adding a 30% buffer to your emergency fund’s target amount if you stick with the default stock/bond allocation. There also may be tax implications should you withdraw funds.

Your decision will again come down to your comfort level with risk. If the thought of seeing your emergency fund’s value dip, even for a second, gives you heartburn, you might consider sticking with a cash account.

Or you can always hedge and split your emergency fund between the two. There’s no wrong answer here!

Remember to go with the (cash) flow

There’s no final answer here either.

Emergency funds naturally ebb and flow over the years. Your monthly expenses could go up or down. You might have to withdraw (and later replace) funds. Or you simply might realize you need a little more saved to feel secure.

Revisit your numbers on occasion—say, once a year or anytime you get a raise or big new expense like a house or baby—and rest easy knowing you’re tackling one of the most important financial goals out there.

Create an emergency fund today.