Investing in Your 20s: 4 Major Financial Questions Answered

When you're in your 20s, you may be starting to invest or you might have some existing assets you need to take better care of. Pay attention to these major issues.

For most of us, our 20s is the first decade of life where investing might become a priority. You may have just graduated college, and having landed your first few full-time jobs, you’re starting to get serious about putting your money to work. More likely than not, you’re motivated and eager to start forging your financial future.

Unfortunately, eagerness alone isn’t enough to be a successful investor. Once you make the decision to start investing, and you’ve done a bit of research, dozens of new questions emerge. Questions like, “Should I invest or pay down debt?” or “What should I do to start a nest egg?”

In this article, we’ll cover the top four questions we hear from investors in their twenties that we believe are important questions to be asking—and answering.

- “Should I invest aggressively just because I’m young?”

- “Should I pay down my debts or start investing?”

- “Should I contribute to a Roth or Traditional retirement account?”

- “How long should it take to see results?”

Let’s explore these to help you develop a clearer path through your 20s.

“Should I invest aggressively just because I’m young?”

Young investors often hear that they should invest aggressively because they “have time on their side.” That usually means investing in a high percentage of stocks and a small percentage of bonds or cash. While the logic is sound, it’s really only half of the story. And the half that is missing is the most important part: the foundation of your finances.

The portion of your money that is for long-term goals, such as retirement, should most likely be invested aggressively. But in your twenties you have other financial goals besides just retirement. Let’s look at some common goals that should not have aggressive, high risk investments just because you’re young.

- Emergency fund. It’s extremely important to build up an emergency fund that covers 3-6 months of your expenses. We usually recommend your emergency fund should be kept in a lower risk option, like a high yield cash account or low risk investment account.

- Wedding costs. According to the U.S. Census Bureau, the median age of a first marriage for men is 29, and for women, it’s 27. You don’t want to have to delay matrimony just because the stock market took a dip, so money set aside for these goals should also probably be invested conservatively.

- A home down payment. The median age for purchasing a first home is age 33, according to the the National Association of Realtors. That means most people should start saving for that house in their twenties. When saving for a relatively short-term goal—especially one as important as your first home—it likely doesn’t make sense to invest very aggressively.

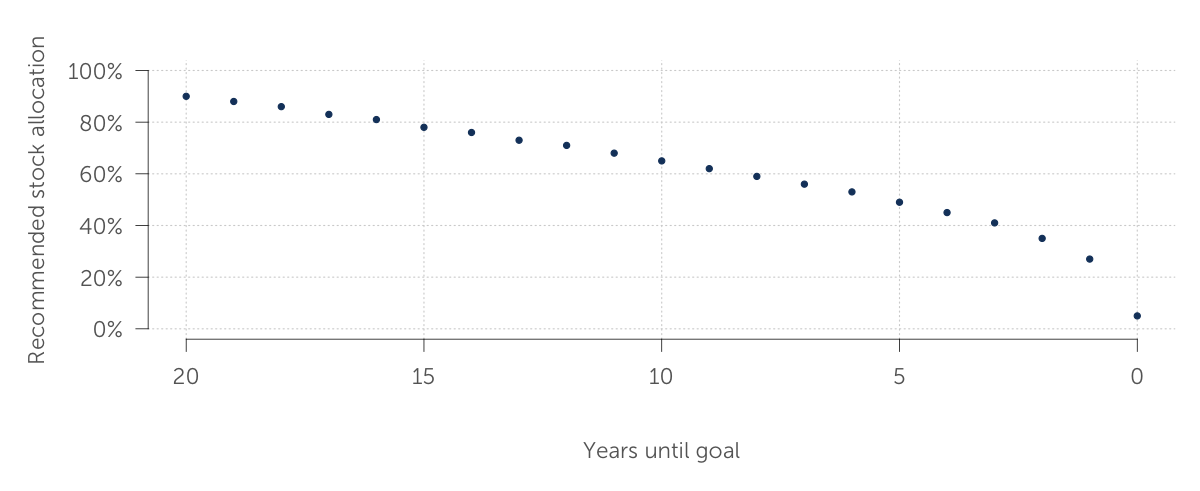

So how should you invest for these shorter-term goals? If you plan on keeping your funds in cash, make sure your money is working for you. Consider using a cash account like Cash Reserve, which is traditionally able to offer interest rates above the national average.

If you want to invest your money, you should separate your funds into different buckets for each goal, and invest each bucket according to its time horizon. An example looks like this.

The above graph is Betterment’s recommendation for how stock-to-bond allocations should change over time for a major purchase goal.

And don’t forget to adjust your risk as your goal gets closer—or if you use Betterment, we’ll adjust your risk automatically, in eligible portfolios.

“Should I pay down my debts or start investing?”

The right risk level for your investments depends not just on your age, but on the purpose of that particular bucket of money. But should you even be investing in the first place? Or, would it be better to focus on paying down debt?

In some cases, paying down debt should be prioritized over investing, but that’s not always the case.

Here’s one example: “Should I pay down a 4.5% mortgage or contribute to my 401(k) to get a 100% employer match?” Mathematically, the employer match is usually the right move. The return on a 100% employer match is usually better than saving 4.5% by paying extra on your mortgage if you’re planning to pay the same amount for either option.

It comes down to what is the most optimal use of your next dollar. We've discussed the topic in more detail previously, but the quick summary is that, when deciding to pay off debt or invest, use this prioritized framework:

- Always make your minimum debt payments on time.

- Maximise the match in your employer-sponsored retirement plan.

- Pay off high-cost debt.

- Build your emergency fund.

- Save for retirement.

- Save for your other goals (home purchase, kid’s college).

“Should I contribute to a Roth or Traditional retirement account?”

Speaking of employer matches in your retirement account, which type of retirement account is best for you? Should you choose a Roth retirement account (e.g. Roth 401(k), Roth IRA) in your twenties? Or should you use a traditional account?

As a quick refresher, here’s how Roth and traditional retirement accounts generally work:

- Traditional: Contributions to these accounts are usually pre-tax. In exchange for this upfront tax break, you usually must pay taxes on all future withdrawals.

- Roth: Contributions to these accounts are generally after-tax. Instead of getting a tax break today, all of the future earnings and qualified withdrawals may be tax-free, if IRS requirements are met.

So you can’t avoid paying taxes, but at least you can choose when you pay them. Either now when you make the contribution, or in the future when you make the withdrawal. As a general rule:

- If your current tax bracket is higher than your expected tax bracket in retirement, you should choose the Traditional option.

- If your current tax bracket is the same or lower than your expected tax bracket in retirement, you should choose the Roth option.

The good news is that Betterment’s retirement planning tool can do this all for you and recommend which is likely best for your situation. We estimate your current and future tax bracket, and even factor in additional factors like employer matches, fees and even your spouse’s accounts, if applicable.

“How long should it take to see investing results?”

Humans are wired to seek immediate gratification. We want to see results and we want them fast. The investments we choose are no different. We want to see our money grow, even double or triple as fast as possible!

We are always taught of the magic of compound interest, and how if you save $x amount over time, you’ll have so much money by the time you retire. That is great for initial motivation, but it’s important to understand that most of that growth happens later in life. In fact very little growth occurs while you are just starting.

The graph below shows what happens over 30 years if you save $250/month in today’s dollars and earn a 7% rate of return. By the end you’ll have over $372,000! But it’s not until year 5 that you would earn more money than you contributed that year. And it would take 18 years for the total earnings in your account to be larger than your total contributions.

How Compounding Works: Contributions vs. Future Earnings

The figure shows a hypothetical example of compounding, based on a $3,000 annual contribution over 30 years with an assumed growth rate of 7%, compounded each year. Performance is provided for illustrative purposes, and performance is not attributable to any actual Betterment portfolio nor does it reflect any specific Betterment performance. As such, it is not net of any management fees. Content is meant for educational purposes on the power of compound interest over time, and not intended to be taken as advice or a recommendation for any specific investment product or strategy.

The point is it can take time to see the fruits of your investing labor. That’s entirely normal. But don’t let that discourage you. Some things you can do early on to help are to make your saving automatic and reduce your fees. Both of these things will help you save more and make your money work harder.

Use Your 20s To Your Advantage

Your 20s are an important time in your financial life. It is the decade where you can build a strong foundation for decades to come. Whether that’s choosing the proper risk level for your goals, deciding to pay down debt or invest, or selecting the right retirement accounts. Making the right decisions now can save you the headache of having to correct these things later.

Lastly, remember to stay the course. It can take time to see the type of growth you want in your account.