Save and earn more with 4.00% APY*

APY is variable.

Grow your savings with a high-yield cash account. Betterment’s Cash Reserve secures your money during volatile times while earning nearly 10x the national average.**

...loading image

Save and earn more with 4.00% APY*

APY is variable.

Grow your savings with a high-yield cash account. Betterment’s Cash Reserve secures your money during volatile times while earning nearly 10x the national average.

-

$0 fees.

Forget any monthly or maintenance costs—what you earn is what you keep. -

$2 million insured.

Rest easy with FDIC insurance up to $2 million ($4 million for joint accounts) with our program banks, subject to certain conditions. That's 8X what most firms offer. -

Unlimited withdrawals.

Compare this to other banks that limit how often you can access your money. -

No minimum balance.

Other institutions offer higher interest rates based on a larger balance—you can grow your money with us for as little as $10.

Optimize your cash today.

Start saving for tomorrow.

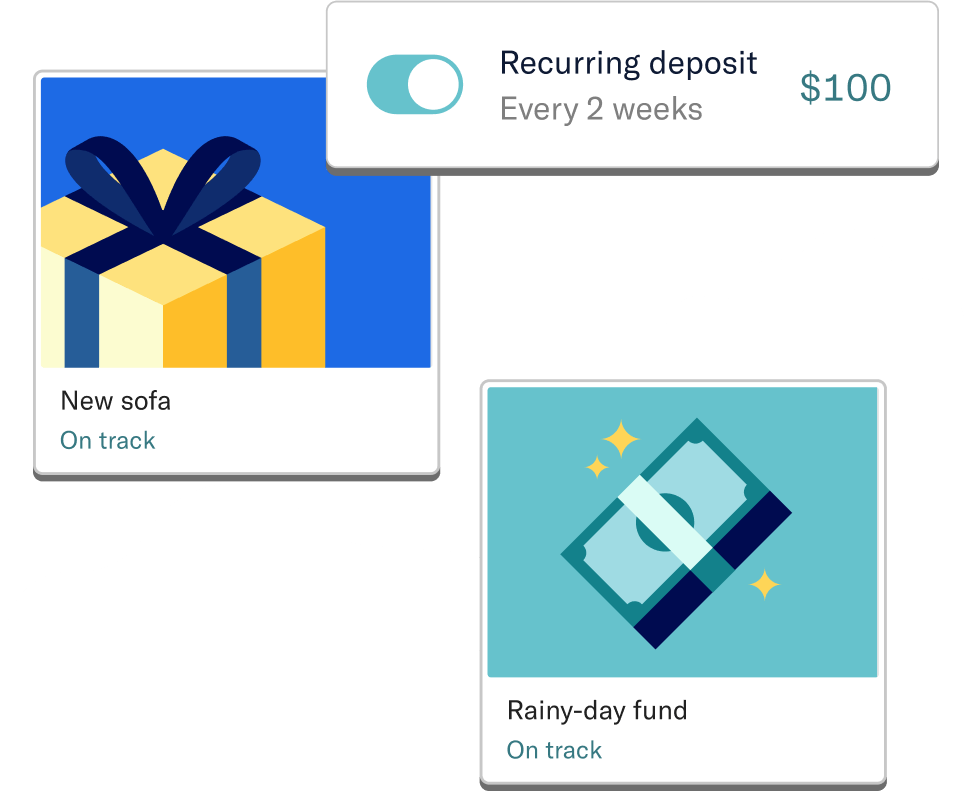

Set money aside for what matters to you. Create multiple savings goals and use our automated tools to help you achieve them.

Keep your money safe as it grows.

Cash Reserve lets you earn interest even during volatile times. FDIC insurance covers your money up to $2 million ($4 million for joint accounts) at our program banks, subject to certain conditions meaning you won’t have to sacrifice security for growth.

Ready to boost your cash?