![]()

What’s new from Betterment Advisor Solutions

Explore the latest updates designed to help you grow client relationships, streamline billing, and deliver more value at scale.

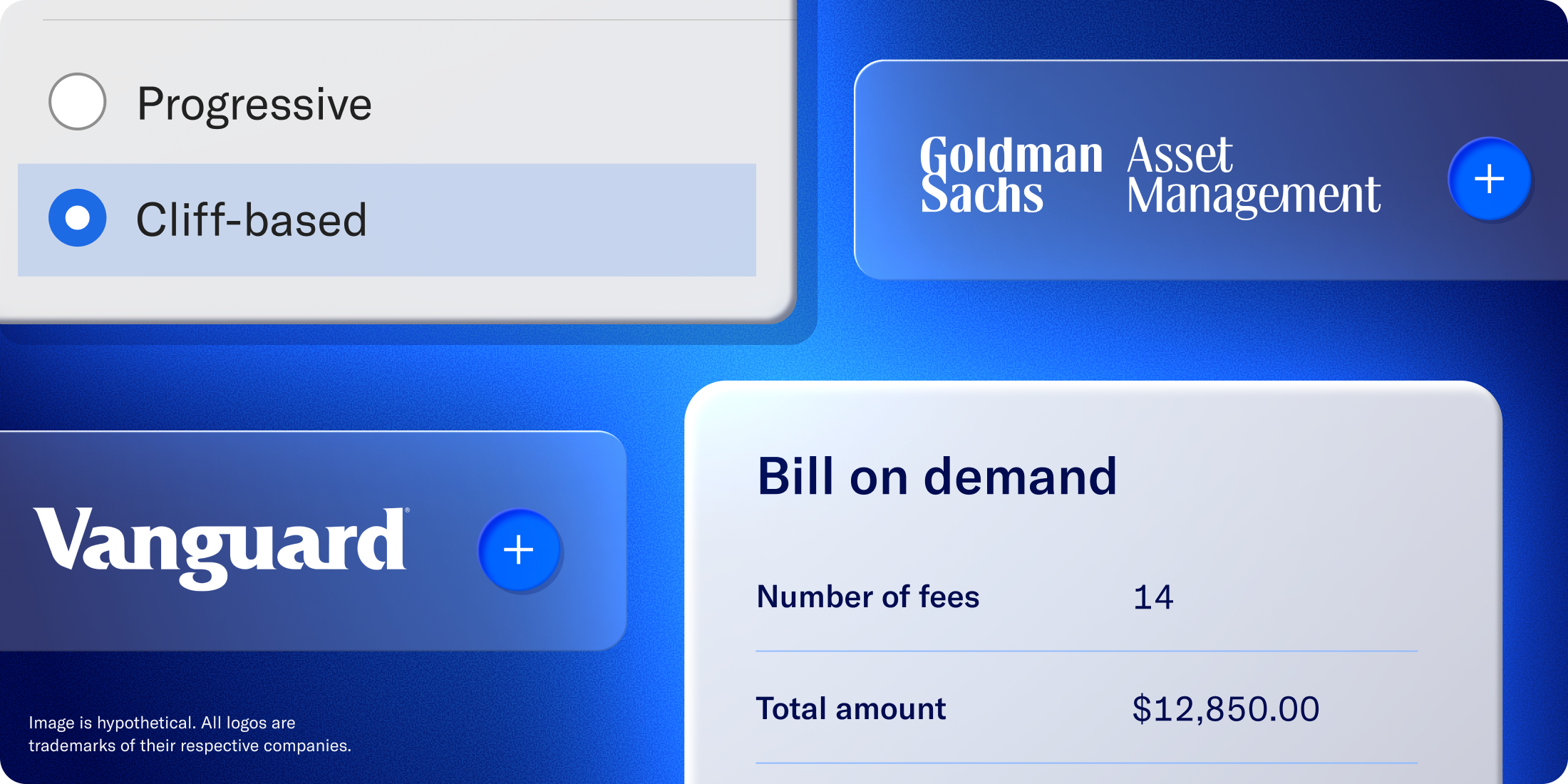

What’s new from Betterment Advisor Solutions true Explore the latest updates designed to help you grow client relationships, streamline billing, and deliver more value at scale. Our latest updates give advisors more ways to grow client relationships at scale, from our expanded model marketplace and smarter billing to new retirement and lending solutions, while driving tax‑efficient outcomes across households. Table of contents Portfolio management Get started with new portfolios from Betterment and other leading asset managers Exit any position effortlessly Help clients earn additional income through securities lending Billing Charge for your added expertise and bill any amount at any time Apply a single tier rate to a client's total AUM Rate mortgage offer Help your clients borrow smarter New integrations Integrate with Nitrogen, Blueleaf and FinDash Retirement Request a new plan proposal within your dashboard Top content How Mach 1 accelerated its growth with a segmentation strategy Explore more options in our model marketplace Give clients more ways to invest with Betterment’s new third‑party model portfolios from industry‑leading asset managers like Goldman Sachs Asset Management, Vanguard, State Street, among others. With the expanded model marketplace, you can: Offer more choice without more operational lift by mapping client preferences to curated, expert‑built models instead of one‑off portfolios. Keep implementation consistent across households, aligning models to your firm’s views on risk, diversification, and brand exposure. Stay tax aware at scale with automated rebalancing, drift controls, and tax-loss harvesting on eligible models. Use these models with our tax-smart technology to drive better outcomes for your clients. Check out the model marketplace Exit any position with ease Now you can sell what you need, when you need it, without disrupting your client’s broader strategy. With increased manual trading capabilities, you can view a client’s holdings by goal or account and sell stocks, ETFs, or mutual funds directly on the platform—in dollars or shares. Proceeds are automatically reinvested into the target portfolio, which helps to keep goals on track while you adjust what no longer fits. Coming soon: Help your clients earn potential income with securities lending Betterment clients will soon be eligible to earn additional income on authorized stocks and ETFs they already hold through our new Fully Paid Securities Lending (FPSL) Program. Through the program, your clients lend fully paid stocks and ETFs from their Betterment account to institutional borrowers—typically for speculation, risk-management, or price discovery. Your clients will share the income generated from these loans, while maintaining economic ownership of their investments including the ability to sell their shares at any time. Learn more Bill in all the ways you need With on‑demand billing, you can charge for planning projects, tax strategy consults, and other one‑off services outside your standard fee schedule—any amount, any time— via file upload directly through your Betterment dashboard. That means a cleaner client experience, and more billing consolidated in one place. With cliff‑based tiered billing, you can build custom breakpoints, set rates, and let the platform handle the rest—automatically repricing fees as household AUM crosses each tier, with no manual intervention required. And, you can reward larger relationships with cleaner discounts or grow smaller accounts more intentionally, all while keeping billing logic centralized in Betterment. Explore billing options Help clients unlock discounted mortgage rates Betterment is partnering with Rate to offer eligible clients access to discounted mortgage pricing. Qualifying clients can get up to 0.75% off their mortgage rate* and $500 off closing costs when they purchase a new home—or have the lender fee waived on a refinance. It’s another way Betterment advisors can support their clients’ major life goals, like homeownership, while deepening planning conversations around cash flow, borrowing costs, and long‑term wealth. Explore the offer today See our new integrations in action Experience more connected workflows across your tech stack with new integrations: Nitrogen: Automatically sync your clients’ Betterment portfolio data into Nitrogen so you can align risk and investment strategy without manual uploads or tab‑hopping. Blueleaf: Keep your clients’ Betterment positions, balances, and transactions current in Blueleaf, giving you clearer reporting and a more complete view of each client’s household. FinDash: Feed your clients’ Betterment data into FinDash’s AI‑powered operating system so your team can turn planning insights into automated, proactive service at scale. View all integrations Request new plan proposals from your dashboard You can now request a new plan proposal directly from the Betterment platform, without having to fill out separate forms. Just click Request for Proposal in your account, enter the plan and client details, and submit. With the new streamlined process, you can move faster on new opportunities. Explore more How Mach 1 scaled small accounts without stretching its team See how Mach 1 Financial Group used Betterment Advisor Solutions to build a segmented service model for smaller and emerging clients, freeing up significant back‑office time while preserving a high‑touch experience for larger relationships. By moving select households onto a digital, automated investing experience powered by Betterment, Mach 1 created a scalable way to serve more clients of all sizes, improve operational efficiency, and keep growth from overwhelming its service team. Read the full case study Log in to explore what’s new, or reach out to your relationship manager if you’d like to take a closer look at any of these features. If you’d like to take a look around with someone from our team, book a demo.