Your future-proof 401(k)

Betterment makes it easy for small and mid-market businesses to provide a scalable retirement plan.

-

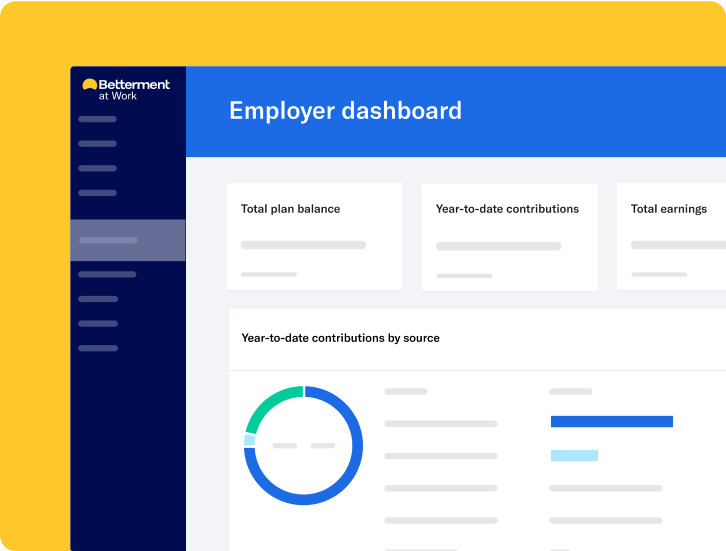

Retirement Assets under Management

-

-

-

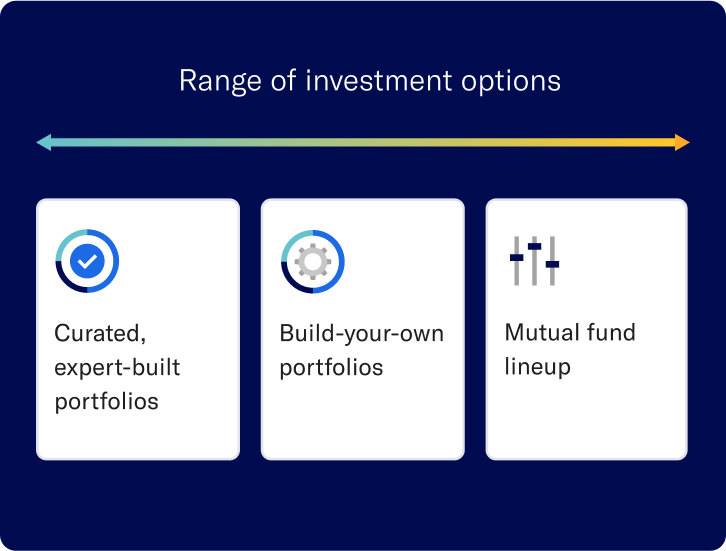

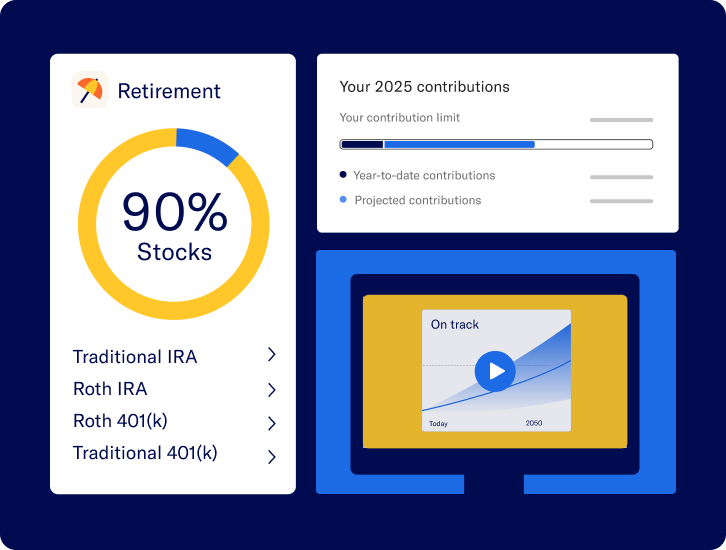

Leverage our track record to deliver a better retirement plan. Provide everything from expert-built, curated portfolios to customizable investment options, giving employees the flexibility to save on their terms.

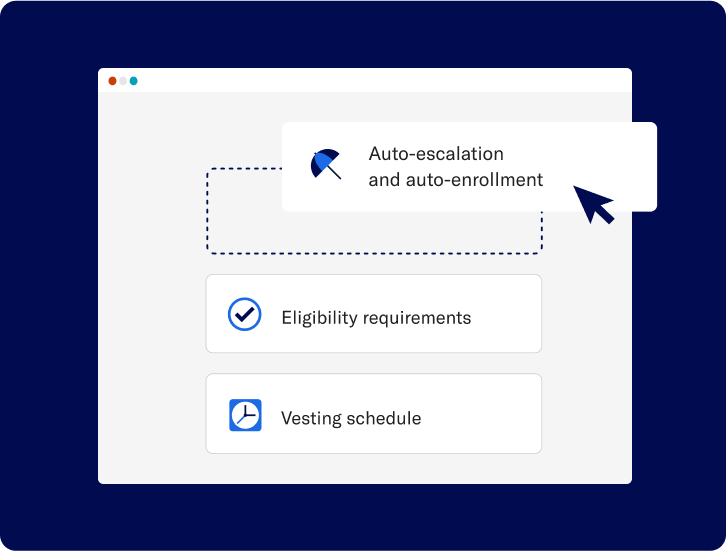

Design a plan that fits your needs, from auto-escalation and auto-enrollment to eligibility requirements, vesting schedule, profit sharing—and much more.

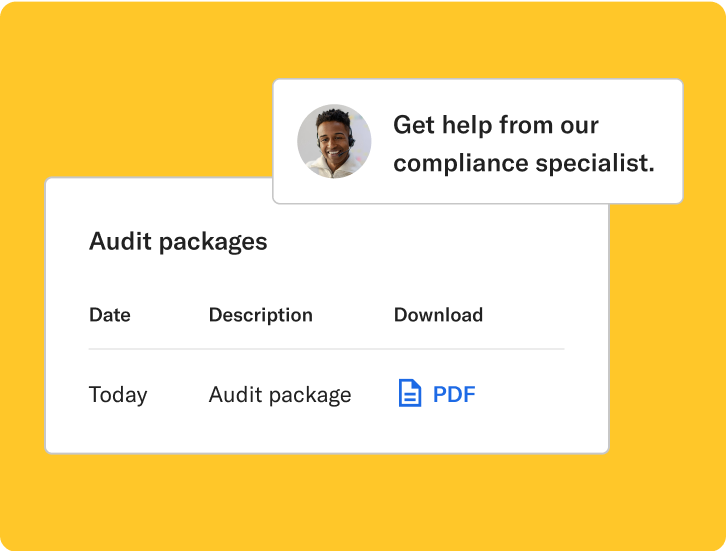

Trade compliance complexity for certainty with our team of specialists who handle annual testing, calculate contributions, and prepare signature-ready Form 5500 to help your plan stay compliant.

Employees can access a wealth of educational resources, including videos, webinars, and articles to answer questions and help them level up their finances. We also engage employees with in-app retirement advice and customized emails covering a range of 401(k)-related topics.

Estimate your plan costs with our tax savings calculator.

Ongoing support for plan sponsors

Employee support team

Specialists are available via call, email, or chat to resolve the specific needs of employees.

An onboarding specialist by your side

Quickly set up your new or conversion plan with support from a dedicated onboarding specialist.

Powered by Betterment.

-

FAQs

Get instant answers to common questions.

-

Book a demo

Get a demonstration of our 401(k)

in action. -

Resources

Go in-depth on specific topics.

-

What is Betterment at Work?

Learn more about what we have to offer.

Launch your 401(k) today.