ESG Investments in 401(k) Plans

The DOL proposal provides clarity with ESG investing.

In the beginning of 2021, the Department of Labor (DOL) released a “final rule” entitled “Financial Factors in Selecting Plan Investments,” pertaining to ESG (environmental, social, governance) investments within a 401(k) plan. In March 2021, the DOL under the Biden administration stated that they were not going to enforce the previous administration’s rule until they had completed their own review. Most recently, the Biden DOL released its own proposal, reworking parts of the rule to be more favorable to the inclusion of ESG investments within 401(k)s and clarifying areas that had a chilling effect on fiduciaries performing their responsibilities.

So what’s changed?

| 2020 Rule | New Proposal | |

|---|---|---|

| Evaluating investments | Investment choices must be based on “pecuniary” factors, which include time horizon, diversification, risk, and return. | Clarifies that ESG factors are permissible and are financially material in the consideration of investments. |

| Qualified default investment alternative (QDIA) | Cannot select investment based on one or more non-pecuniary factors. | ESG factors are permissible, allowing the possibility of wider adoption of ESG funds and portfolios. |

| Tie-breaker test (when deciding between investments) | Non-financial factors such as ESG are permissible. However, they must have detailed documentation. | Permitted to select investments based on “collateral benefits” such as ESG. Where collateral benefits form the basis for investment choice, disclosure of collateral benefits required. Detailed tie-breaker documentation not required. |

| Proxy voting | Fiduciaries are not required to vote every proxy or exercise every shareholder right. | Revised language stresses the importance of proxy voting in line with fiduciary obligations. |

| Special monitoring for proxy voting when outsourcing responsibilities. Proxy voting activities must be recorded. | Additional special monitoring is not required. Removal of record keeping of proxy activities. | |

| Safe harbors: a fiduciary can choose not to vote proxy if (a) the proposal is related to business activities or investment value (b) percentage ownership or the proposal being voted on is not significant enough to materially impact. | Removal of safe harbors. | |

| Voting to further political or social causes “that have no connection to enhancing the economic value of the plan's investment” through proxy voting or shareholder activism is a violation. | Opens the door to ESG factors when voting proxies as under the proposed rule that they are economically material. |

Why is this important?

Under the proposal, the DOL clarifies that “climate change and other ESG factors can be financially material and when they are, considering them will inevitably lead to better long-term risk-adjusted returns, protecting the retirement savings of America’s workers.”

Under the previous rule, many ESG factors would not count as a “pecuniary” factor. However, in actuality ESG factors have a high likelihood of impacting financial performance in the long run. For example, climate change can shift environmental conditions, force companies to transition and adapt to these shifts, lead to disruptions in business cycles and new innovations, and ultimately be a material financial risk over time when a company declines from failing to adapt. For retirement plans, the DOL’s revised proposal acknowledges that ESG risks could be important to consider when reviewing investments for strategic portfolio construction.

Driving impact through ESG investing and proxy voting works. We’ve seen this concept in action with Engine No. 1 winning three ExxonMobil board seats in a six month long proxy battle. The change in having three new board members that are conscious of climate change and favor transitioning away from fossil fuels will benefit the company in the long term as renewable energy grows in prominence. After its successful proxy battle with Exxon, Engine No. 1 reported cordial discussions with representatives of Chevron Corp. regarding the company’s emissions reduction strategy, and also has reportedly built a stake in General Motors and expressed support for GM’s management actions relating to increased electric vehicle production and GM’s long-term strategy. Ernst & Young also published data showing an increasing trend of how more Fortune 100 companies are incorporating ESG initiatives into proxy statements. For example, 91% disclosed they are incorporating workplace diversity into their initiatives in 2021 versus 61% in 2020.

Demand for ESG products will continue

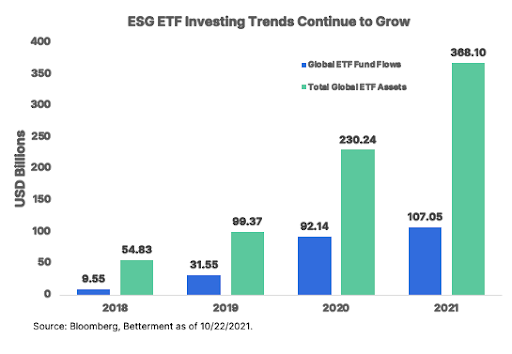

We believe demand for ESG-focused investing will continue to grow, and it is important that regulations are clarified to accommodate this trend. Bloomberg projects that global assets in ESG will exceed $50 trillion by 2025, which is significant as it will represent a third of projected global assets under management. In the US, $17 trillion is invested in ESG assets. Trends within ESG ETFs tell the same story where fund flows this year have increased by more than 1000% compared to flows seen just three years ago.

How Betterment incorporates ESG investing in 401(k) plans

At Betterment, we believe investing through an ESG lens matters, and can be important to 401(k) participants investing on a longer time horizon. We’ve found many ways to thoughtfully weave ESG investing into our portfolio strategies.

Betterment has a 10+ years track record of constructing globally diversified portfolios, along with a history of implementing ESG investment strategies in 401(k)s using our Socially Responsible Investing (SRI) portfolios. The SRI portfolios come with three different focuses: Broad Impact, Social Impact, and Climate Impact. Each of these portfolios allow our clients to choose how they want to invest to best align their portfolio with their values.

Perceptions of higher fees in the ESG investment space has been a misconception that has historically posed an obstacle to the adoption of pro-ESG regulation. Expense ratios of ESG ETFs have declined to 0.20%, which is low compared to the 0.47% average expense ratio of all ETFs in the US. Within Betterment’s SRI portfolios, and depending on the investor’s overall portfolio allocation to stocks relative to bonds, the asset weighted expense ratios of the Broad Impact, Social, and Climate portfolios range from 0.12-0.18%, 0.13-0.20%, 0.13-0.20% respectively.

Another misconception is that in order to adopt ESG investing, you have to sacrifice performance goals. As a 3(38) investment fiduciary, Betterment reviews fund selection on an ongoing basis to ensure we’ve performed our due diligence in selecting investments suitable for participants' desired investing objectives. To determine if there were in fact any financial tradeoffs associated with an SRI portfolio strategy relative to the Betterment Core, we examined evidence based on historical returns. When adjusting for the stock allocation level and Betterment fees, we found that:

- There were no material performance differences.

- The portfolios were highly correlated overall.

- In certain time periods the SRI portfolios outperformed the Betterment Core portfolio.

Another example of how we’ve incorporated ESG impact investing is through the addition of the Engine No. 1 Transform 500 ETF (VOTE) into all three of our SRI portfolio strategies in 2021. With VOTE ETF, you can still maintain exposure to the 500 largest companies within the US at an inexpensive expense ratio of 0.05%. That may seem counterintuitive since it mirrors owning the S&P 500 Index, however the magic happens behind the scenes as the fund manager uses share ownership to vote proxies in favor of ESG initiatives. This is a new form of shareholder activism and another way performance goals, exposure, and fees do not have to be sacrificed to make a difference.

What’s next?

We are hopeful that ease of interpretation with this rule may allow wider adoption of ESG products as investment options and may lead to greater incorporation of ESG factors in the decision making process as we do believe they are material. This has been a focus of Betterment’s as we seek to remain ahead of the trend with our product solutions.

We will continue to monitor ongoing developments and keep you informed.

Note: Higher bond allocations in your portfolio decrease the percentage attributable to socially responsible ETFs.