How AI is disrupting software stocks in 2026

AI coding tools are driving a wedge between broad tech and software-only funds. Here's what the divergence means for client portfolios. Software has a problem. It’s called AI.

For all of the technology’s dazzling displays of prose, picture-generation, and problem solving, code is very much its most fluent language. As of April 2026, Google reported that human-generated code has dwindled to 25%.

Tech companies with their own AI products are well-positioned in this environment. They own the tools to automate software engineering and can directly profit from others doing the same.

Smaller software companies, however, face a more precarious outlook. The mere prospect of a DIY software future has turned investor sentiment against the Software as a Service (SaaS) businesses, raising predictions of a “SaaSpocalypse” in the process. Why pay for expensive enterprise software when you can build it yourself in-house?

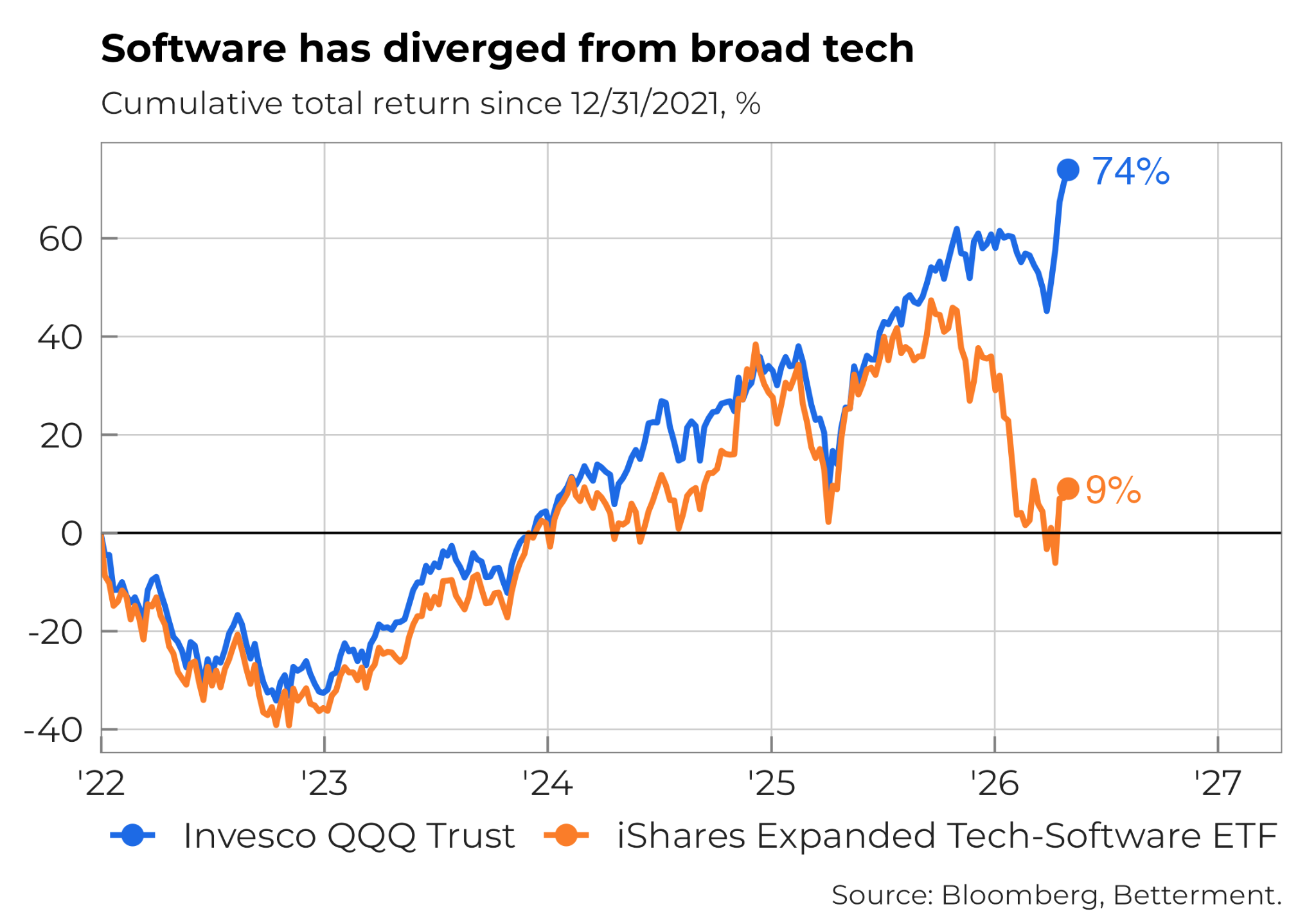

To see this trendline in action, look no further than two funds: Invesco QQQ Trust (QQQ) and iShares Expanded Tech-Software Sector ETF (IGV).

QQQ is made up of the 100 biggest non-finance companies listed on the Nasdaq stock exchange. Filtering out financial firms means it’s heavily concentrated in broad-based technology companies like Alphabet (Google), Amazon, and Microsoft—all mighty players in the AI investment boom.

IGV, meanwhile, primarily holds the software industry, including Salesforce, Adobe, and Intuit. While many of them are racing to integrate AI into their products themselves, they don’t own the underlying technology.

These two funds have historically moved in lockstep. As goes software, so goes the broader technology sector. At least until recently. Something snapped late last year, and that correlation broke down.

That something was Claude Code, an AI coding tool from Anthropic that went mainstream in late 2025. Its significance for markets lies in what it signaled: AI “agents” could soon handle complex workflows that businesses currently pay SaaS to manage.

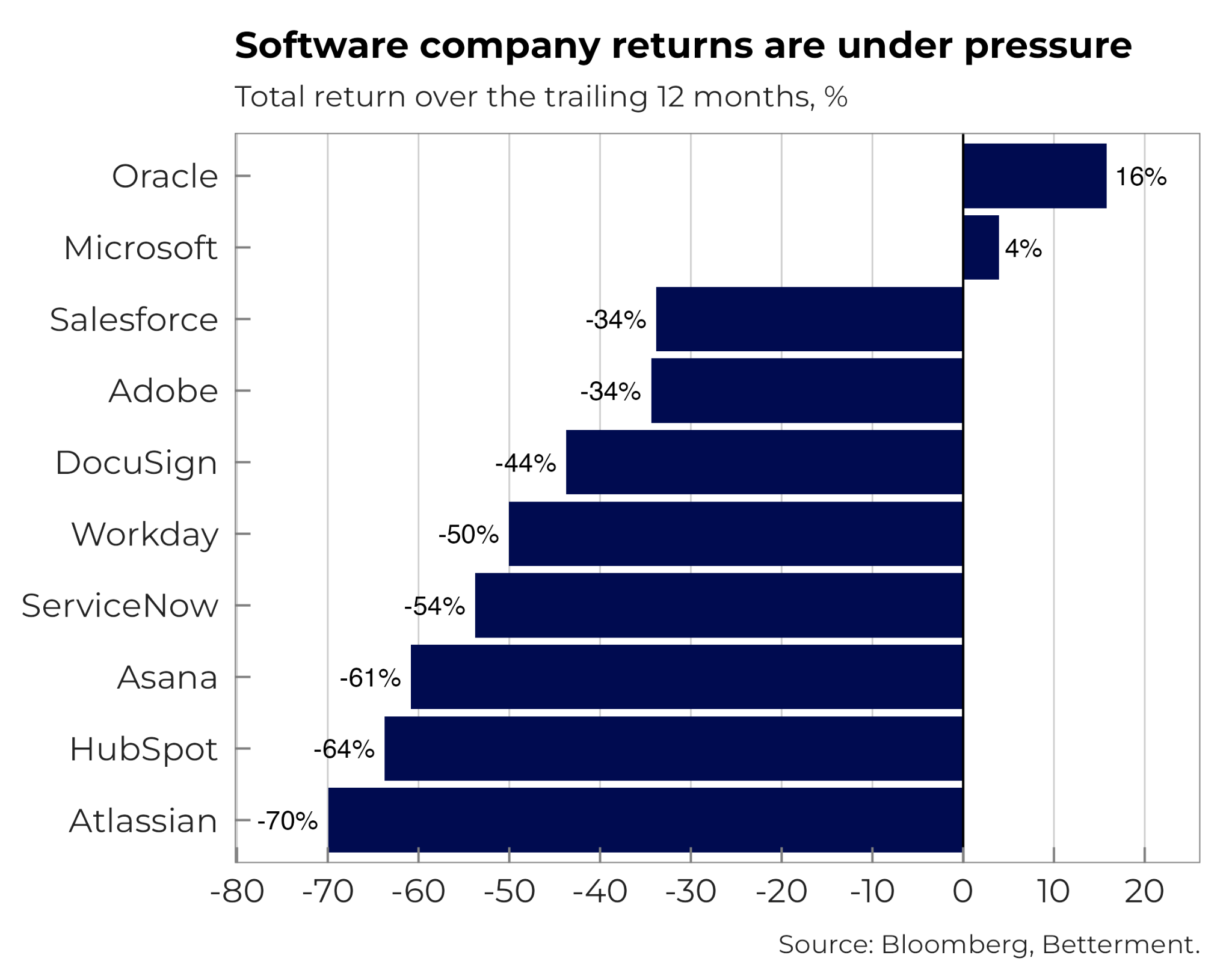

The investment research firm Citrini added fuel to the fire in February 2026, with the release of“The 2028 Global Intelligence Crisis," a report that imagined a near future where AI agents steal the market share of not just SaaS companies—but major tech and finance firms, too. For all of its alleged shortcomings in sound macroeconomic thinking, the paper went viral and moved markets. Taken all together, software stocks have experienced significant downturns over the last 12 months.

With valuations in the software space having reset considerably, there may now be more cushion against further downward price pressure. Many of these businesses are also actively adapting their models—so, it would be premature to count them out.

The chart below compares the price-to-earnings ratios currently to those at the beginning of 2025 for a sample of the largest software companies in the world. Stocks like Adobe and Salesforce are trading at a 50% discount now relative to early 2025, based on this valuation metric.

More generally, with all of these uncertainties and headwinds out there for sectors like software, why is the market near all-time highs? Some of that resilience may reflect investor momentum, but the more fundamental explanation lies in strong corporate earnings growth.

More generally, with all of these uncertainties and headwinds out there for sectors like software, why is the market near all-time highs? Some of that resilience may reflect investor momentum, but the more fundamental explanation lies in strong corporate earnings growth.

The primary source of investment returns over the long-term is growth in net income—companies' ability to become more profitable. Even as the war in Iran has been going on, analysts have revised their 2026 earnings growth estimates upwards. That's true across the board, with the U.S. as well as firms in Europe, Japan, and emerging markets forecasted to see an acceleration in profit growth. In spite of the headwinds from the conflict in Iran, this earnings backdrop remains a meaningful tailwind for clients holding diversified portfolios with a long-term investment horizon.