Your future-proof 401(k)

Betterment makes it easy for small and mid-market businesses to provide a scalable retirement plan. With a Betterment 401(k), you get:

- Simplified administration, payroll integration, fiduciary support, and compliance testing

- Customizable plan features and optional employee benefits

- Service and support at every step

- All-in pricing with no hidden fees

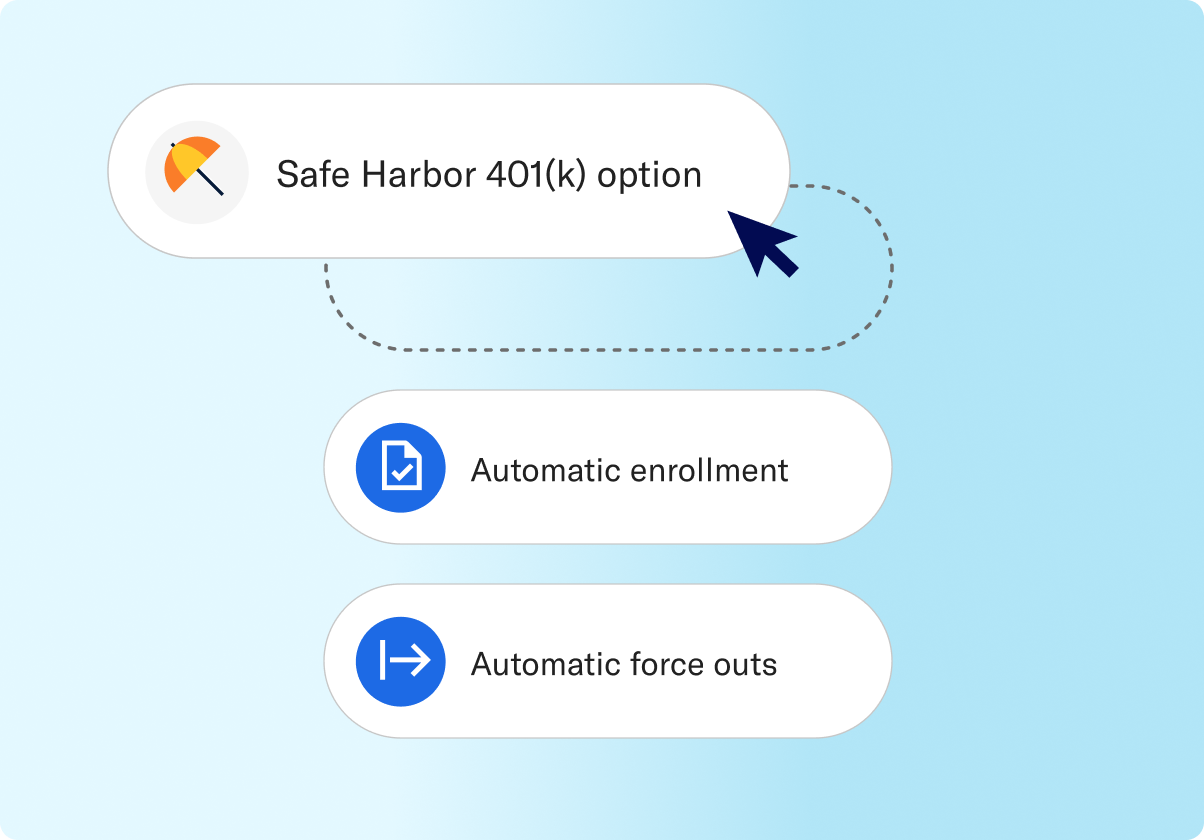

Customizable plan design to fit your needs.

Whether you're starting or leveling up your 401(k), our flexible plan features let you achieve your business goals while supporting your employees.

- Eligibility requirements

- Vesting schedule

- Profit-sharing

- Safe Harbor 401(k) option

- Automatic enrollment

- Automatic escalation

- Automatic force outs

- 401(k) match on student loan payments Learn more

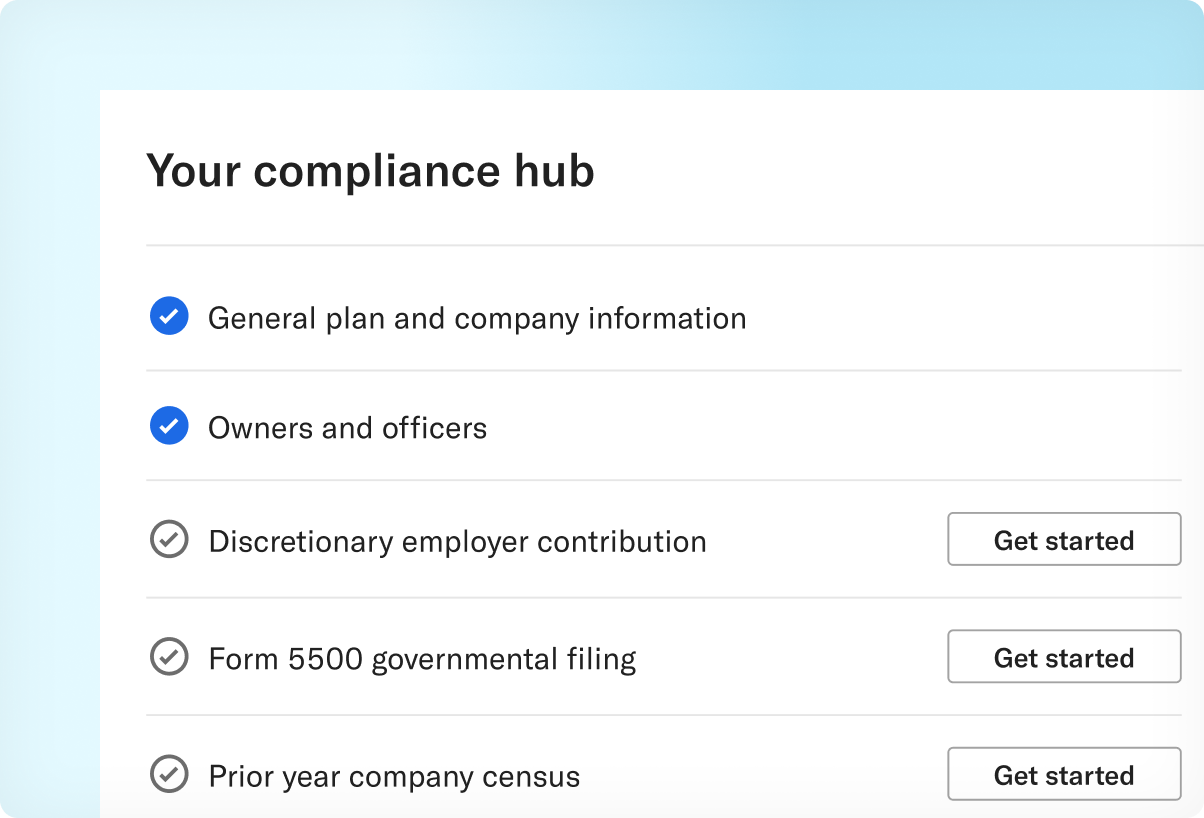

Administrative and compliance support at every step.

We handle regulatory filings and monitor your plan to help resolve any potential compliance issues.

- 3(16) and 3(38) fiduciary responsibility

- Prepare Form 5500 for compliance

- Service and live support for you and your employees

partners in compliance

The Hassle-Free Compliance Guarantee

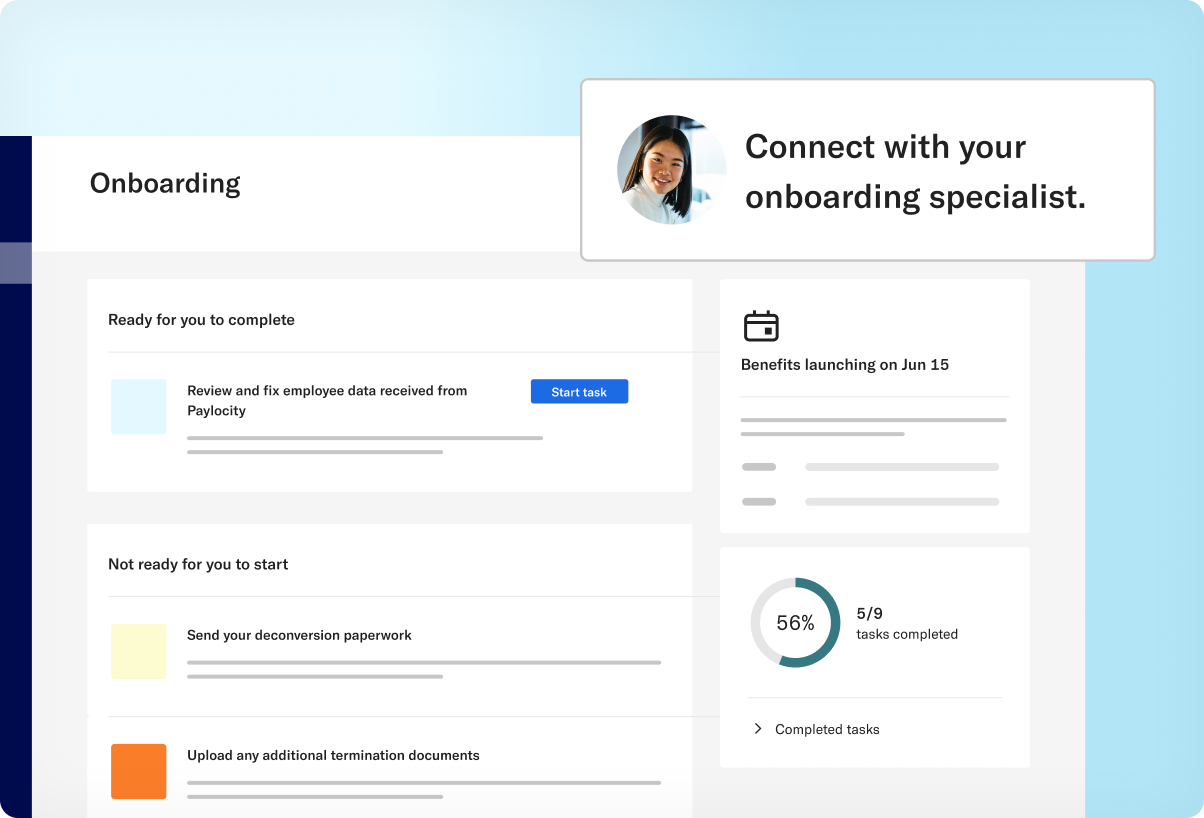

Dedicated onboarding support.

Set up your new or conversion plan with the help of an onboarding specialist.

-

15%

faster plan conversion onboarding with Betterment compared to the industry average.

Betterment at Work was a no-brainer. Administratively, it’s incredibly user-friendly. New employees are able to set up their 401(k) immediately and it syncs with the payroll platform, saving us time.

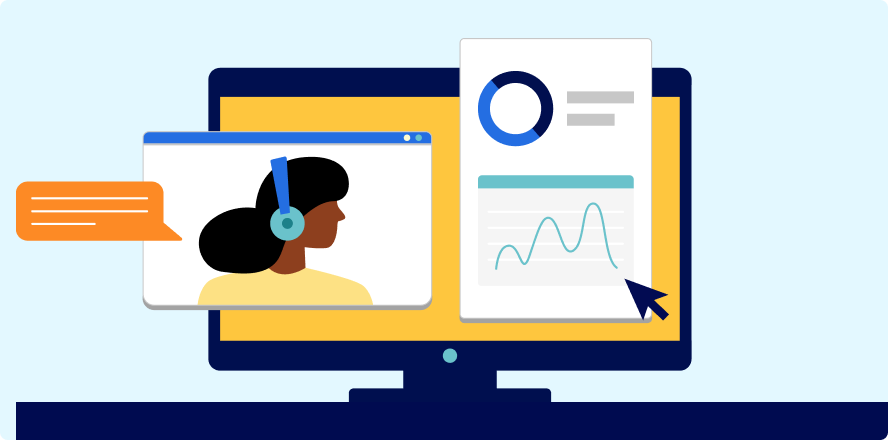

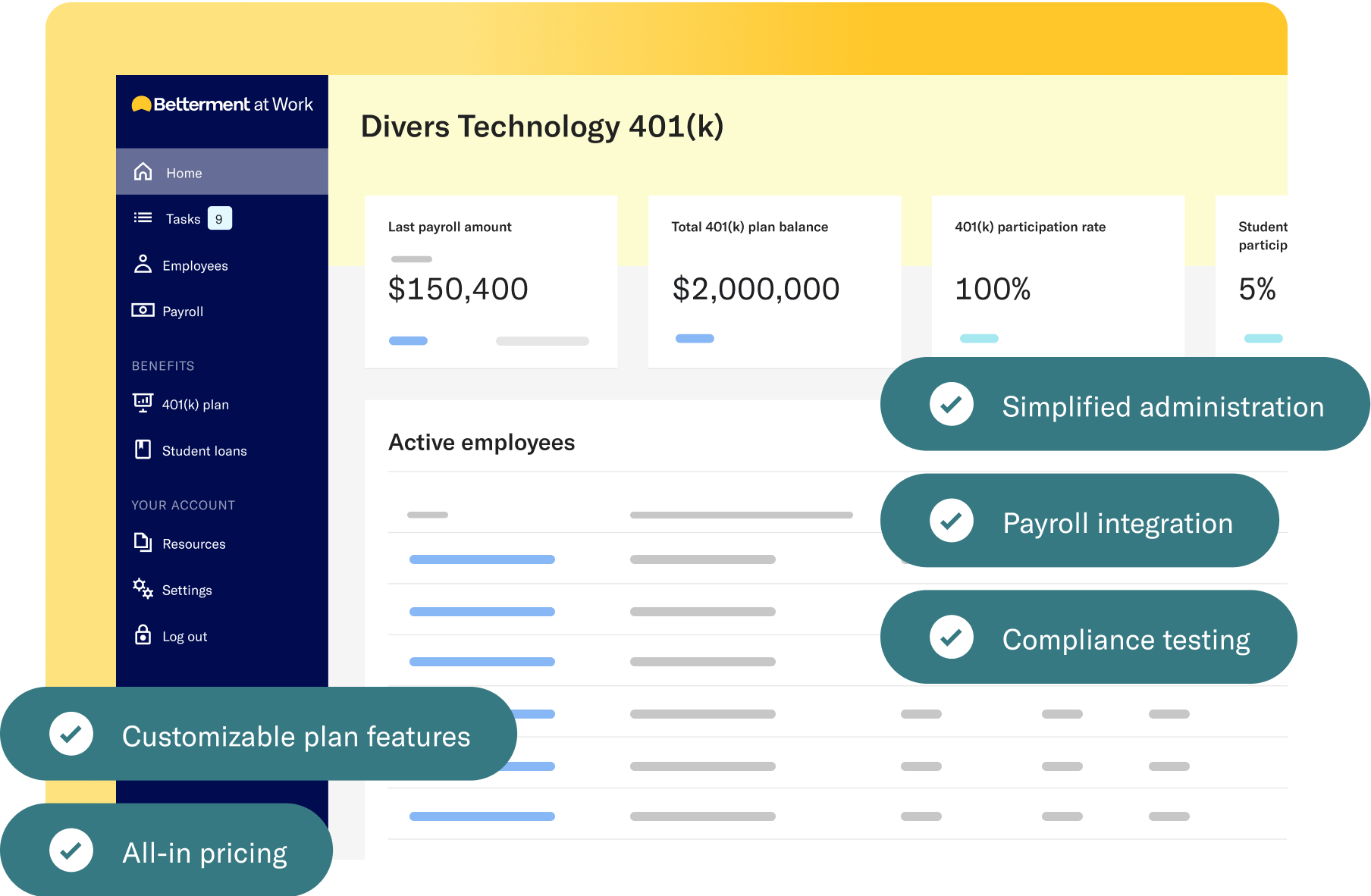

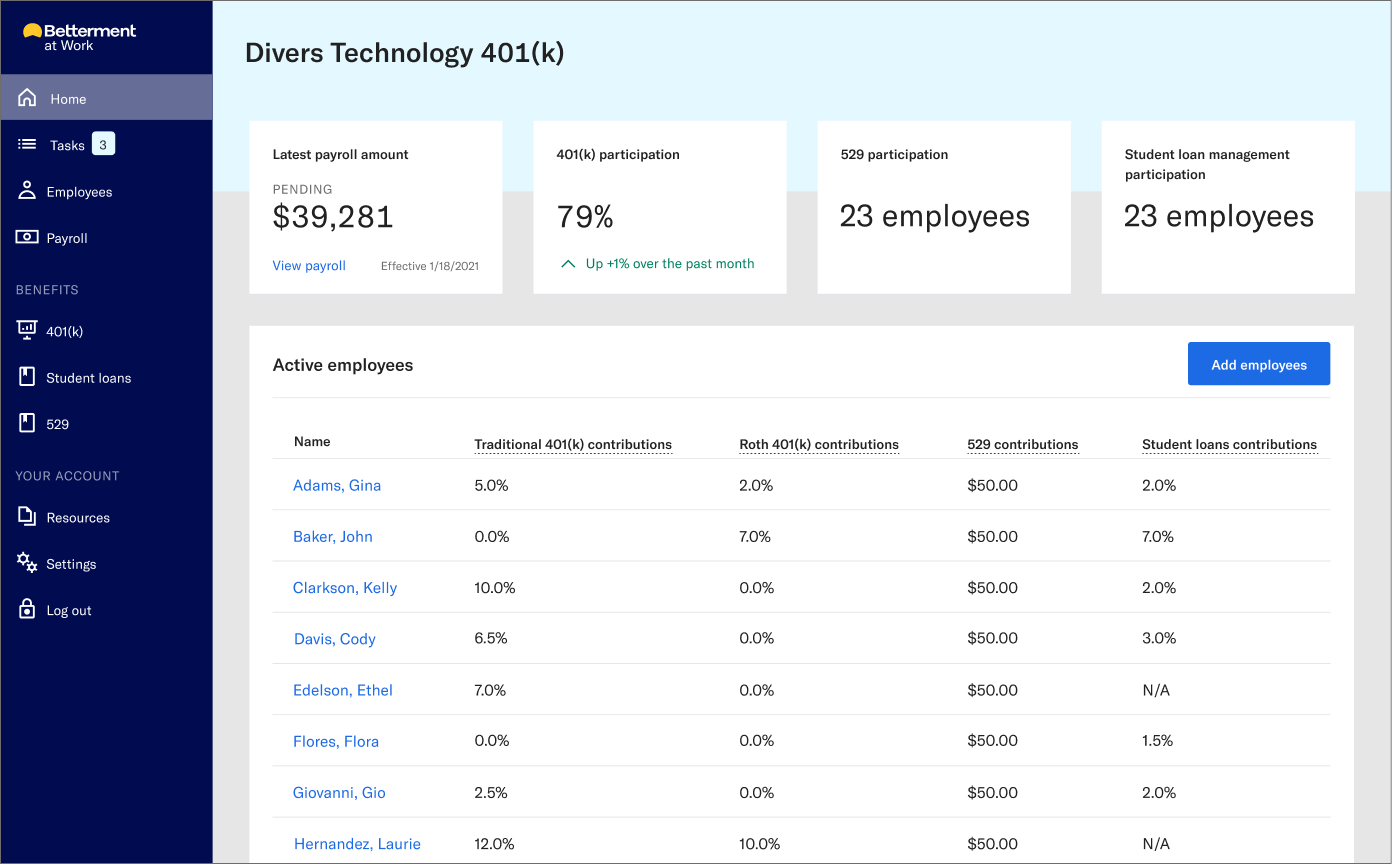

Seamlessly administer your 401(k) from an all-in-one dashboard.

- Real-time plan insights.

Track plan metrics, generate custom reports, and get participant-level data with just a few clicks. - Resources at your fingertips.

Access one-pagers, webinar registrations, articles, and videos for you and your employees. - Simplified compliance hub.

Actively monitor your plan’s compliance status and projected test results.

Engage and empower

your employees.

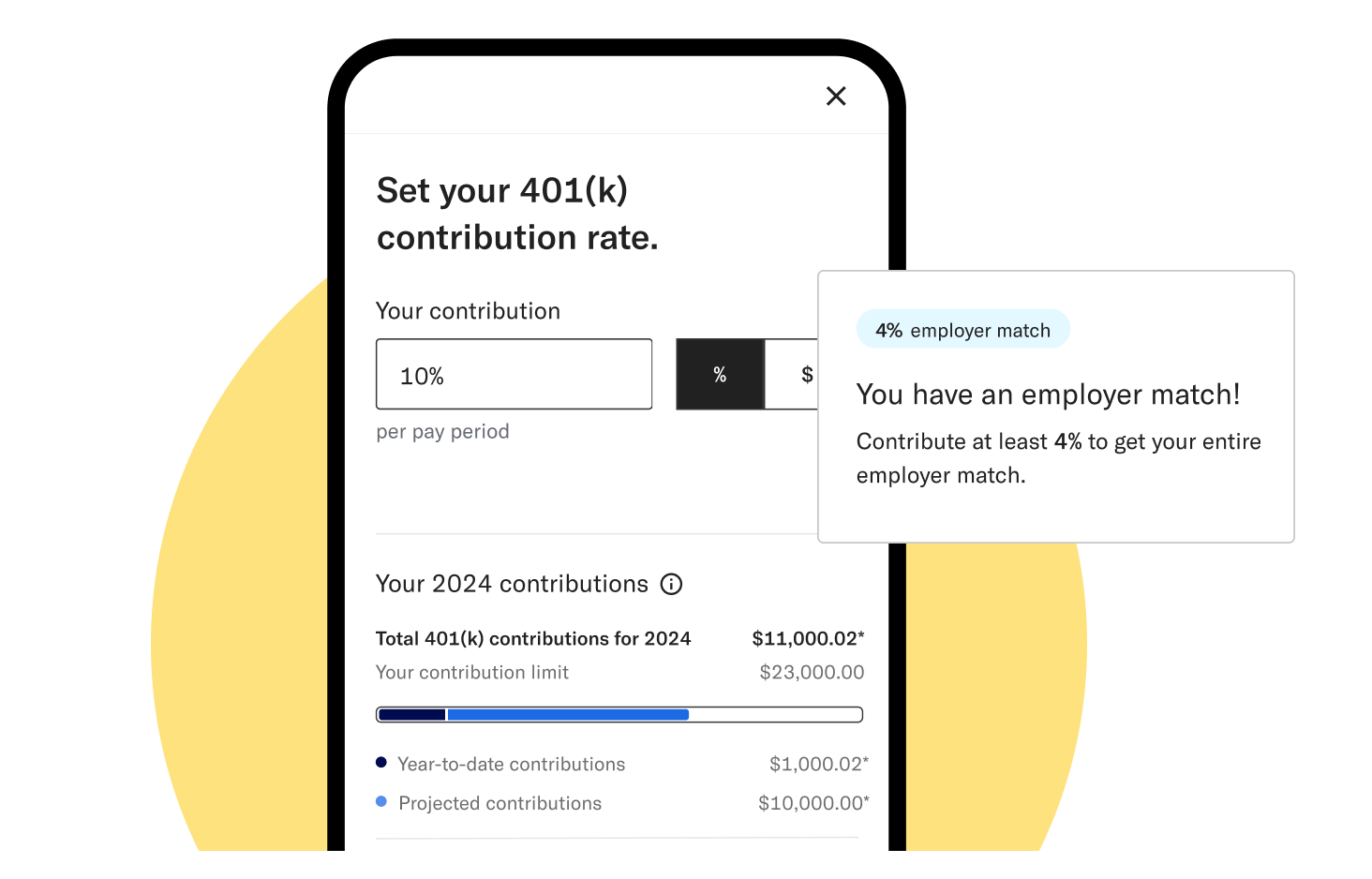

Get the technology and features to help employees achieve what they want with their money.

- Delightful and highly-rated app

- Access to tax-advantaged IRAs

- Support and educational resources

4.7 rating

60,500§ reviews

See full disclosures for award details.

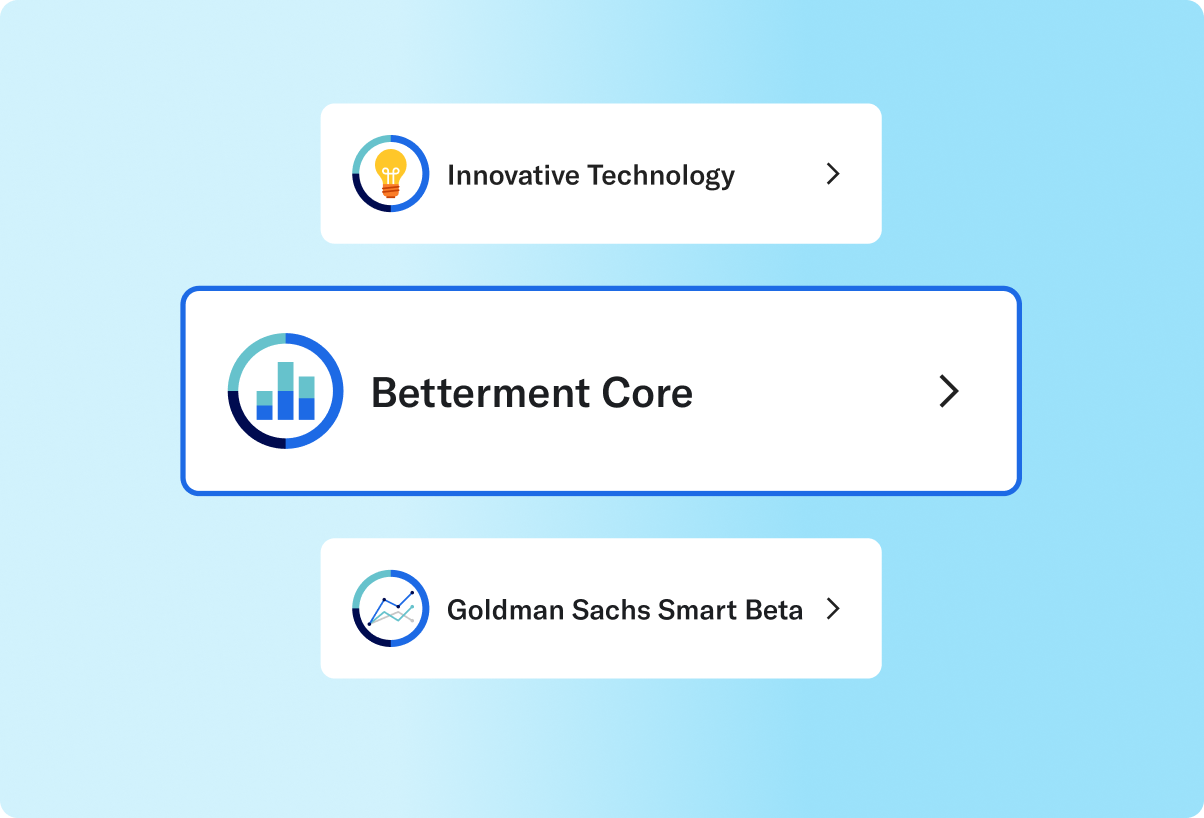

Curated, expert-built portfolios to invest in.

Our diversified portfolios make investing easy for employees. They can choose the portfolio that interests them, from sustainability to innovative technology.

More experienced investors can customize their asset class weights. All portfolios are built by experts using generally low-cost exchange-traded funds.

-

Financial Coaching

Offer employees unlimited 1:1 financial advice and planning sessions with our team of financial advisors.

-

Student Loan Management

Help your team tackle student debt with loan tracking, repayment guidance, and an optional match.

-

529 Education Savings

Make saving for education simple for employees with automated payroll deductions and an optional match.

-

401(k) match on student loan payments

A first-to-market offering: Broaden plan participation by offering a 401(k) match to payments made on qualified student loans.

Powered by Betterment.